The Impact of Internal Corporate Governance Mechanisms on Profitability in Companies Listed in the Stock Market

This paper attempts to investigate the effects of the internal corporate governance mechanisms represented in (the size of the board of directors, CEO duality, the administrative ownership, and the ownership of Block Shareholders Ownership) on the profitability of the companies listed on the Egyptian Stock Exchange. The sample of the study reached (85) companies listed on the Egyptian Stock Exchange for the period 2012 to 2016. The researcher relied on the method of "Moment Structures Analysis (AMOS) Of Analysis to study the relationships between the study variables. A program specially prepared by Dr. Andrew F. Hayes is to test the direct effects of the sub-elements of one variable on the sub-elements of another variable. The methodology of this method depends on the Sobel test and the Bootstrap method. The research has reached several results, the most important of which are: There is a positive, statistically significant impact relationship between the internal corporate governance mechanisms with its various dimensions and profitability, and the researcher has recommended that companies should strive to comply with corporate governance rules and support internal corporate governance mechanisms because of their positive impact on profitability.

Introduction

The business and financial environment witnessed a number of failures and financial and moral corruption as a result of the weak role of corporate governance systems, which in turn affected the rights of shareholders due to bankruptcy and liquidation. The most prominent thing that the recent financial crisis made clear at the beginning of 2008 is the emphasis on the importance of an effective financial management and strengthening Corporate governance practices [1], and effective financial management decisions such as (maintaining liquidity and solvency) are essential functions to create competitive advantages [2].

Corporate governance is defined as a set of mechanisms, procedures, laws, systems and decisions that guarantee discipline, transparency and fairness, and thus aims to achieve quality and excellence in performance by activating the actions of the economic unit management in relation to the exploitation of the economic resources available to it, thus achieving the best possible benefits for all stakeholders and society As a whole [3].

The concept of corporate governance has been linked to the financial crises and collapses that occurred in various parts of the world, which had their effects on harming the rights of shareholders due to bankruptcy and liquidation cases. Specialists have confirmed that these crises were the result of wrong behaviors passed through weak legislation, laws and ineffective risk management [4]. This made many countries work to enact laws and adopt procedures that call for improving corporate governance systems, and activating their internal and external tools. Accordingly, a number of countries have adopted some governance tools to monitor the management’s actions and decisions related to shareholder wealth, including determining the number of board members, and periodically electing a board of directors from shareholders, in addition to emphasizing the separation between the CEO and the chairman’s job.

The interest in governance emerged after the rise of huge investments that require separation between stakeholders and those who manage these investments, so it was imperative that there be a law that links and regulates the relationship between the parties, so the interest in corporate governance began as it is a system that controls corporate business and distributes rights and duties between various parties in companies [5].

The interaction and effectiveness of internal corporate governance tools, including (ownership by members of the board of directors, ownership by Block Shareholders Ownership of the company’s shares and the size of the board of directors) can play a positive role in controlling management behavior and its actions and achieving harmonization between corporate profitability and liquidity within the framework of achieving synchronization between cash inflows and outflows in order to avoid the company For financial hardship cases.

There is a difference in the impact of internal governance mechanisms (board size, duplication of the CEO’s role, administrative ownership, ownership of Block Shareholders Ownership) on the performance of companies as there are many studies indicating that the size of the board of directors has some effect on the Performance of companies, however there are opinions. However, some researchers have indicated that a smaller board size is more effective in monitoring, controlling and setting decisions [6, 7]. In contrast, a study Mollah, et al. [8] found that a larger board of directors It is better and more effective due to the diversity of the wide range of experiences among managers.

Hashim, et al. [9] emphasized the necessity of separating the role of the chairman of the board of directors and the role of the chief executive, in order to avoid the concentration of power in one person and the possibility of exercising the required supervision and control over the work of the management, and that the combination of the two roles harms the independence of the board because of the existence of different roles For both of them. Whereas, the Stewardship theory sees the combination of the role of the CEO and the chairman of the board of directors leading to the enhancement of the decision-making process [10].

There are studies indicating that the ownership structure is one of the main mechanisms that affect the performance of companies. Shuto, et al. [11] indicated that although the agency theory suggests that administrative ownership helps achieve convergence between the interests of managers and shareholders, that Administrative ownership leads to a kind of conflict between shareholders and the interests of bondholders, which causes the owner-manager of the company to make investment and financing decisions that maximize their own benefit at the expense of bondholders.

Therefore, it is noted that there is an increase in the interest of governments and financial institutions in governance as a solution through which they can be implemented to create a set of guiding controls to improve their performance as a result of the administrative, economic and political pressures they are exposed to due to the expansion of the volume of activities, the movement of capital across borders, and the weakness of supervision and control over them. In addition to the occurrence of many economic collapses and successive financial crises.

In light of the previous presentation, the study problem can be identified in the following main question: - What is The Effect of Internal Governance Mechanisms on Profitability in Companies Listed on The Egyptian Stock Exchange?.

Literature Review

Mukhtar, et al. [12] aimed to test the relationship between the characteristics of the board of directors, the ownership structure and the performance of companies in the companies listed on the Egyptian Stock Exchange. The researcher used the size of the board of directors and the dual roles to measure the characteristics of the board of directors. He also used government ownership, administrative ownership, institutional ownership and concentration of ownership to measure the ownership structure. The companies’ performance was measured by each rate of return on assets, rate of return on ownership, Tobin Q index and the ratio of market value to book value. The research sample reached 50 of the most active companies in the Egyptian stock market during the period from 2008 to 2011. The research found a positive statistically significant relationship between the size of the board of directors, government ownership and the performance of companies. The results also indicate the existence of an inverse statistically significant relationship between Dual roles and corporate performance.

Azzoz, et al. [13] aimed to find out the effect of corporate governance characteristics on the quality of profits and profit management. The research sample included all financial companies listed on the Amman Stock Exchange and the number of companies reached 73 companies for the period from 2007 to 2012, and the researcher used the number of board members, the duplication of the president. The executive, the formation of the board of directors, the number of members of the audit committee, the components of the audit committee and the activity of the audit committee to measure the characteristics of corporate governance, and the research found a positive and moral relationship between (size of the board - duality of the executive director) and the rate of return on property rights, and the research recommended financial companies By reducing the number of board members, and adjusting the percentage of external and non-executive directors in both the board of directors and the audit committee.

Tsagem, et al, [5] indicated the effect of working capital management (WCM), family or family ownership, and the size of the board of directors on profitability in small and medium enterprises in Nigeria, and the researcher used the financial reports of a sample that included 235 SMEs in Nigeria (160 companies). Family-owned, 75 companies not owned by family members) for the period between 2008 - 2012, and the research found conflicting and inconclusive results about the relationship between the size of the board of directors and the performance of companies, as Jensen, et al. indicated that the small board of directors is more effective in management and control. And decision-making, and this is what both Kumar, et al. [7] and Ujunwa, et al. [6] have also reached. On the other hand, Abor, et al. [14] found that the size of a large board of directors is better and more effective due to the presence of great diversity and wide experiences among managers. Mollah, et al, [8] indicated that the size of the large board of directors tends to be more powerful for the control of the CEO, and this is also indicated by the study Qureshi, et al. that there is a positive relationship between the size of the board of directors and the performance of companies.

Manasir, et al. [15] found by analyzing sample data that included (153) companies for the three years from 2009 - 2011, and (21) companies were excluded due to the absence of the minimum acceptable level of data, as the research concluded that there is no significant impact Statistical significance for the application of corporate governance rules as a whole on both the return on assets (ROA) and the return on equity (ROE) for Jordanian public services companies, and the researcher recommended the need to pay attention to the application of governance rules related to shareholders’ rights because of their impact on the return on assets and the return on share. the one.

While the study Ajanthan, et al. [16] went to identify the effect of the internal mechanisms of corporate governance (size of the board, family ownership, percentage of female presence in boards of directors) on the performance and profitability of companies, as it reached through application on a sample of (18) companies for the period from 2007 - 2012 indicated that there is a positive relationship between the size of the board and the profitability of the company, and that there is a positive relationship between corporate governance practices and the profitability of these companies.

The study Ujunwa, et al. [6] also dealt with the relationship between the characteristics of the board of directors and the financial performance of Nigerian companies, and the research aimed to identify the effect of the characteristics of the board of directors (size of the board, skills of the board of directors, nationality of the board of directors, gender, race, double chief executive) on financial performance To companies. The researcher used a sample consisting of (122) companies listed on the Nigeria Stock Exchange for the period 1991-2008. The research found that each of (CEO dualism, diversity in gender) was negatively correlated with the performance of the companies, in contrast, it was found that each of (the nationality of the board of directors, the race, the number of board members who have PhD qualifications) correlated positively with the performance of the companies.

Through the application on a sample that covered 30 companies for the period between 2003 -2007, Heenetigala, et al. [17] addressed the relationship between corporate governance rules and corporate performance. Governance was measured through (separation between the chairman of the board of directors and the executive director, the formation of the board of directors) and was measured. Financial performance through (return on assets, return on equity), and where the research found a positive relationship between corporate governance and the performance of companies, as the results indicated an increase in profit and share price performance in companies that implement corporate governance strategies.

In another context Yahyaoui, et al. [18] aimed to shed light on the role of corporate governance in improving the financial performance of companies, and to know the concept of corporate governance, its objective, the parties concerned with it, as well as its basics and principles, and then its role in improving financial performance. The research found a set of results, the most important of which is that companies that implement corporate governance become more attractive to investors, which leads to increased access to capital markets, credit period, lower cost of financing, increased market value of the company, reduced risks and increased competitiveness of the company, and faced corruption and capital flight .

While Ezzine, et al. [19] tried to analyze the impact of corporate governance mechanisms on the performance of Saudi companies during the recent financial crisis, and the research sample included 96 companies listed in the Saudi market during the period from 2007 to 2008. The research concluded that there is an inverse relationship between the size of the board of directors and the separation between the positions of Chairman and CEO with share price performance.

In Light of the Analysis of these Studies, the Following is Evident

There is variation and disagreement about the impact of corporate governance on the performance and profitability of companies, as the study of Tsagem, et al. [3] and Azzoz, et al. [13] concluded that there is a related relationship between corporate governance and corporate profitability, and as that the efficiency of corporate governance has an impact on the relationship between working capital management and corporate profitability, and this is what Musleh, et al. also found.

While Ahmed, et al. [20] concluded that there is no positive relationship between the various internal mechanisms of corporate governance stipulated in the principles of Egyptian corporate governance and the performance indicators of the selected companies. Manasir, et al. [15] indicated that there is no statistically significant effect of applying the rules of corporate governance as a whole to all From return on assets (ROA), and return on equity (ROE) for Jordanian public service companies. It has been found from previous studies that there is a difference in the impact of internal governance mechanisms (board size, CEO duplication, administrative ownership, ownership of Block Shareholders Ownership) on the performance of companies as:

There are many studies indicating that the size of the board of directors has some impact on the performance of the companies, however there are conflicting opinions while some researchers have indicated that the small board of directors is more effective in monitoring, controlling and setting decisions Kumar, et al. [7].

In contrast, my studies Abor, et al. [14] and Mollah, et al. [8] found that a larger board of directors is better and more effective given the diversity of a wide range of experiences among managers.

Hashim, et al. [9] indicated the necessity of separating the role of the chairman of the board of directors and the role of the CEO, in order to avoid the concentration of power in one person and the possibility of exercising the required supervision and control over the work of the management, and that the combination of the two roles would harm the independence of the board because of the existence of roles Different for each. Whereas, the Stewardship theory sees the combination of the role of the CEO and the chairman of the board of directors leading to the enhancement of the decision-making process [21, 22, 23, 24, 25, 26, 27, 28, 29, 30, 31, 32, 33, 34, 35].

There are studies indicating that the ownership structure is one of the main mechanisms that affect the performance of companies and where James, et al. pointed to the benefits of establishing family- owned companies due to their characteristics such as altruism, trust and patriarchy that create love and commitment for men. Business and that the establishment of family companies provides a system of corporate governance, especially to reduce costs and improve performance, and that such companies are less likely to fail than others. On the other hand, the study Shuto, et al. [11] indicated that although the agency theory suggests that administrative ownership helps to achieve convergence between the interests of managers and shareholders, yet administrative ownership leads to a kind of conflict between shareholders and bondholders’ interests. This conflict drives the company’s owner-manager to make investment and financing decisions that maximize their own benefit at the expense of the bondholders [36, 37, 38, 39, 40].

Research Hypotheses

There is a statistically significant significant impact relationship between internal governance mechanisms and profitability.

This hypothesis is divided into the following sub- hypotheses: - H1: There is a positive statistically significant impact relationship between board size and profitability. H2: There is a positive statistically significant impact relationship between CEO role and profitability. H3: There is a positive statistically significant impact relationship between managerial ownership and profitability. H4: There is a positive statistically significant impact relationship between major shareholder ownership and profitability.

Search Methodology

Research Community

The research community is represented by all the companies listed on the Egyptian Stock Exchange, the number of which according to the Egyptian Stock Exchange website is 222 companies in various sectors [41, 42].

The Research Sample

Given the lack of all corporate governance data for all companies listed in the Egyptian stock market, the research sample consisted of a simple random sample chosen from the Egyptian companies listed in the Egyptian stock market, during the period between 2012 and 2016, and the research sample was (85) A company and provided that these companies meet the following conditions [43, 44].

The selected companies must be listed on the Egyptian Stock Exchange from 1/1/2012 until 12/31/2016.

That the companies selected are non-financial and non- service industrial companies, and thus the following are excluded:

- Banking and financial services sectors, with the exception of banks, due to the different nature and corporate governance system for these sectors.

- That the required data be available during the search period for all companies selected in the research sample, which are represented in: annual financial statements, ownership structure, formation of the board of directors.

The following table shows the descriptive statistics of the study sample data, which includes (85) companies listed in the Egyptian stock market for a time series for the financial period from 2012 to 2016, with a total number of observations reaching (425) (Table 1). The table includes a number of statistical measures: The lowest value, the highest value, the mean, and the standard deviation for each of the study variables, as follows [45, 46, 47, 48, 49, 50].

| Dimensions Of The Variables | Minimum | The Highest Rate | Arithmetic Mean | Standard Deviation | |

|---|---|---|---|---|---|

| Internal corporate governance mechanisms (Independent variable | Board size | 3 | 71 | 1 | 7220 |

| Internal corporate governance mechanisms (Independent variable | Duplicate the CEO role | 0 | 7 | 50 | 7240 |

| Internal corporate governance mechanisms (Independent variable | Administrative ownership (%) | 0 | 30 | 0 | 7220 |

| Internal corporate governance mechanisms (Independent variable | Block Shareholders Ownership (%) | 0 | 30 | 1 | 7220 |

| Profitability (Dependent variable) | Rate of return on assets (%) | 70071- | 3307 | 1015 | 20 |

| Profitability (Dependent variable) | Total operating profit (%) | 72070- | 0 | 2015 | 209 |

Table 1: Descriptive statistics of the study sample.

It is noted from the previous table No (1) that: The internal governance mechanisms (the size of the board of directors - the duplication of the role of the executive director - the administrative ownership - the ownership of Block Shareholders Ownership) we find that the arithmetic mean of the size of the board of directors B size (7) and the minimum (the upper limit) for the size of the board of directors is 3 (15), which is not Consistent with what is indicated in the Guide to the Rules and Standards of Corporate Governance in the Arab Republic of Egypt for the year 2011, that the number of members of the Board of Directors shall not be less than (5) members. We find that the arithmetic mean of the CEO Duality duality reached (0.56), indicating that more than 50% of the companies representing the research sample have duplication, meaning that the CEO in these companies is the same as the Chairman of the Board of Directors. We also find that the mean of both the administrative ownership (MO) and the ownership of Block Shareholders Ownership (BSO) was (0.44, 0.27), respectively, which indicates that the ownership structure in the companies representing the research sample depends largely on management’s ownership over the ownership of Block Shareholders Ownership [51].

With regard to the dependent variable, which is profitability (rate of return on assets, gross operating profit), we find that the average rate of return on assets (ROA) and the average rate of gross operating profit (GOP) amounted to approximately (7.8, 8.8), respectively.

Research Hypothesis Test

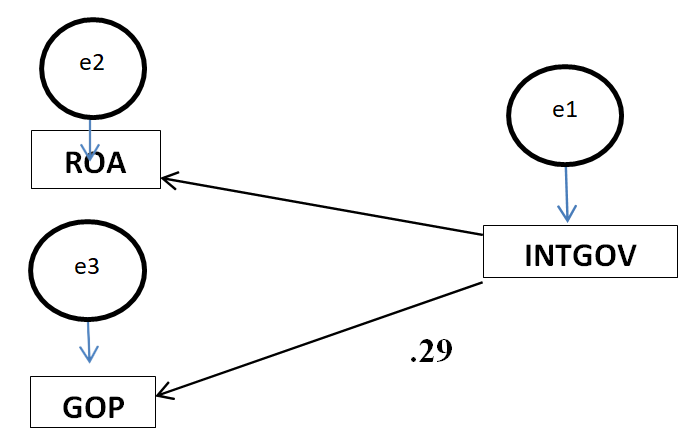

The results of the research and hypothesis testing were divided into: Results on the total level of the variables, followed by the results of the analysis of the influential relationships between the sub-dimensions of the variables included in the study model, and the details of these results are as follows: To test the relationships between the variables of the research model on the overall level, the research model and the influential relationships between the research variables were tested using the modeling of structural equations using the method of “Moment Structures (AMOS) Of Analysis. Figure 1 shows the parameter values of the influencing relationships between the variables of the search model.

Figure 1: Parameters of relationship path analysis for the proposed research model variables. Where: (INTGOV internal governance mechanisms, rate of return on assets (ROA), total operating profit (GOP), outside measurement variables ( E1, E2, E32…) The direct overall effect of the variable “INTGOV internal governance mechanisms” on both the rate of return on assets (ROA) and the total operating profit (GOP) is its coefficient (0.30, 0.29), respectively, and this means that the variance in the variable “internal corporate governance mechanisms” INTGOV) explains By the amount of the previous values of the variance in the profitability variable, and Table 2 shows the total effects between the research variables and (Z) test of the path parameter and their significance (Table 2).

| Variables | Effect | Variables | Path parameter | Standard error | T value | Sig. |

|---|---|---|---|---|---|---|

| INTGOV | ROA | 20 | 20282 | 80 | 0 | |

| INTGOV | GOP | 29 | 20669 | 90 | 0 |

Table 2: Estimates of the path parameters between the model variables and their significance. Sig. using Bootstrap Confildence, b

In light of the data presented in Table 2, the research results indicate the existence of a positive and significant impact relationship of (0.290.0.30) for the internal governance mechanisms as a total variable on profitability (ROA, GOP).

Examining the impact of sub-variables of internal governance mechanisms on profitability_:_ A specially designed program has been relied upon by Dr. Andrew F. Hayes is to test the direct effects of the sub-elements of one variable on the sub- elements of another variable. The methodology of this method depends on the Sobel test and the Bootstrap method, as shown in the following Table 3.

| Sub Variables | Impact factor | Z | Sig. | |||

|---|---|---|---|---|---|---|

| ROA | GOP | ROA | GOP | ROA | GOP | |

| Board size | 355550 | 355060 | 8518 | 8588 | 35333 | 35333 |

| CEO duality | 353531 | 353058 | 5583 | 506 | 353315 | 35331 |

| Managerial Ownership | 351553 | 351010 | 55680 | 55008 | 35333 | 35333 |

| Block Shareholders Ownership | 351015 | 351555 | 5388 | 5500 | 353331 | 35333 |

Table 3: Prepared by the researcher as a result of statistical analysis.

By Looking at Table 3 there is a significant positive impact of the size of the board of directors on profitability (ROA, GOP), where the impact factor was approximately (23.0 and 0.25) respectively, and this means that the difference in the size of the board of directors explains (23.0, 0.25) of the variance in Profitability (ROA and GOP) respectively, and the values of the (z) test and its significance indicate that this overall effect was significant at 95% confidence and significance (0.000).

There is a significant positive impact of the dual role of the CEO on profitability (ROA, GOP), where the impact factor was approximately (05.0, 0.04), respectively, and this means that the difference in the duality of the CEO role explains (05.0, 0.04) of the variance in profitability (ROA and GOP) respectively. The values of the (z) test and its significance indicate that this overall effect was significant with 95% confidence and significance (0.0015).

There is a significant positive impact of administrative ownership on profitability (ROA, GOP), where the impact factor was approximately (15.0 and 0.13), respectively, and this means that the difference in administrative ownership explains (15.0, 0.13) of the variance in profitability (ROA and GOP respectively, and the values of the (z) test and its significance indicate that this overall effect was significant at 95% confidence and significance (0.000).

There is a significant positive impact of the ownership of major shareholders on profitability (ROA, GOP), as the impact factor was approximately (13.0 and 0.12) respectively, and this means that the difference between Block Shareholders Ownership explains (13.0, 0.12) of the variance in profitability. (ROA and GOP). Respectively, and the values of (z) test and its significance indicate that this overall effect was significant with 95% confidence and significance (0.0001).

Summary and Concluded Remarks

internal governance mechanisms have a positive impact on profitability (ROA, GOP), and these results are consistent with the study of Tsagem, et al, [5]; Azzoz, et al. [13]. Manaseer, et al. [15] in light of the previous studies presented that dealt with the relationship between internal governance and profitability, the researcher concluded the following.

The Board of Directors is one of the effective internal governance mechanisms that can contribute to reducing agency problems, while the effectiveness of the Board of Directors depends on forming the board and preventing duplication of roles. Through previous studies, it was found that internal governance mechanisms can affect the efficiency of companies ’performance. And increasing its profitability, as well as separating the management, plays an important role in making decisions that serve the interests of shareholders and all other parties, as it prevents the manager from possessing all powers and making decisions that serve his interests.

Concentration of ownership is one of the effective mechanisms of corporate governance that contributes to reducing agency problems, as the concentration of ownership in the hands of a small number of shareholders prompts them to effectively exercise their supervisory role.

Administrative ownership is one of the mechanisms that reduces agency costs by achieving convergence of interests between managers and shareholders.

Recommendations

In order to achieve benefit from the practical research results, we review, during the following points, a set of recommendations directed to financial managers and the management of joint stock companies listed on the Egyptian Stock Exchange, as follows: -

For the Company’s Board of Directors

Egyptian shareholding companies must adhere to the number recommended in the Egyptian corporate governance rulebook that the size of the board of directors should not be less than 5 members, as the larger board of directors is better and more high due to the diversity of the existence of a wide range of experiences among managers, and as the research found the existence of Positive relationship between board size and profitability.

It is necessary to take into account the separation of the roles of the CEO and the Chairman of the Board of Directors so that the powers do not come together in the hands of one person, which negatively affects the interests of the company, the shareholders and all the other parties, as the current research has found a combination between the role of the CEO and the Chairman of the Board of Directors, even if the results of the research reached a relationship Positive but positive, low impact relationship between CEO role and profitability.

As for the Property Structure

Companies should be keen on the need to achieve a balance in the ownership structure so that members of the board of directors have ownership in the company, which contributes to achieving convergence of interests and reducing administrative opportunism, which was confirmed by the research results of the high percentage of administrative ownership in the companies, the research sample, and its positive impact on profitability. Giving more attention to individual investors, so that the shareholders do not lose part or all of their supervisory rights in the company.

References

-

Kajananthan R, Achchuthan S (2013) Corporate Governance Practices and Its Impact on Working Capital Management: Evidence from Sri Lanka. Research Journal of Finance and Accounting 4(3): 23-31.

-

Ivanovic B, Bogdan k (2011) Corporate Governance Practices and Its Impact on Working Capital Management. Research Journal of Finance and Accounting 7(2): 53-32.

-

Nassar, Wajih A, Hafeez A (2013) The Impact of Applying Corporate Governance Mechanisms on Information Content in the Stock Market: An Applied Study. The Scientific Journal of Economics and Trade 1: 467-493.

-

Al Sartawi, Muttalib A, Musleh M (2015) The Impact of Corporate Governance on the Performance of Companies Listed in the Financial Markets of the Gulf Cooperation Council Countries. Jordanian Journal of Business Administration 11(3): 705-723.

-

Tsagem MM, AripinN, Ishak R (2015) Impact of Working Capital Management, Ownership Structure and Board Size on the Profitability of Small and Medium- Sized Entities in Nigeria”, International Journal of Economics and Financial Issues 5: 77-83.

-

Ujunwa A (2012) Board characteristics and the financial performance of Nigerian quoted firms. Corporate governance 12(5): 656-674.

-

Kumar N, Singh JP (2013) Effect of board size and promoter ownership on firm value: Some empirical findings from India. Corporate Governance 13(1): 88-98.

-

Mollah S, Al Farooque O, Karim W (2012) Ownership structure, corporate governance and firm performance: Evidence from an African emerging market. Studies in Economics and Finance 29(4): 301-319.

-

Hashim HA, Dev S, (2009) Board characteristics, ownership structure and earnings quality: Malaysian evidence. Research in Accounting in Emerging Economies 8: 97-123.

-

Al Midani, Ezzat MA (2004) Corporate Finance Management. Riyadh: Obeikan Library.

-

Shuto A, Kitagawa N (2011) The Effect of Managerial Ownership on the Cost of Debt: Evidence from Japan. Journal of Accounting, Auditing & Finance pp: 590-918.

-

Mukhtar, Saeed A (2016) Study and Test of the Relationship Between Board Characteristics, Ownership Structure and Corporate Performance: The Case of Companies Listed in the Egyptian Stock Market. Journal of Accounting Thought 20(4): 53-106.

-

Azzoz A, Khamees B (2016) The Impact of Corporate Governance Characteristics on Earnings Quality and Earnings Management: Evidence from Jordan. Jordan Journal of Business Administration 12(1): 187-207.

-

Abor J, Biekpe N (2007) Corporate governance, ownership structure and performance of SMEs in Ghana. Implications for financing opportunities. Corporate governance 7(3): 288-300.

-

Manasir Issa O (2013) The Impact of Applying Corporate Governance Rules on the Performance of Jordanian Public Service Companies. Unpublished Master Thesis, the Hashemite University, Jordan.

-

Ajanthan A (2013) Impact of Corporate Governance Practices on Firm Capital Structure and Profitability: A Study of Selected Hotels and Restaurant Companies in Sri Lanka. Research Journal of Finance and Accounting 4(10): 115-127.

-

Heenetigala K, Armstrong A (2012) The impact of corporate goverance firm performance in an unstable economic and political environment: evidence from sri lanka”, financial markets and corporate goverance conference.

-

Naima Y, Hakima B (2012) The Role of Institutional Governance in Improving Corporate Financial Performance. The National Forum on: Corporate Governance as a Mechanism to Reduce Financial and Administrative Corruption, Mohamed Khaider University, Biskra.

-

Ezzine H (2011) A Cross Saudi Firm Analysis of the Impact of Corporate Goverence On Stock Price Performance During The Recent Financial Crisis. European Journal of Economics, Finance and Administration Sciences 43: 137-154.

-

Ahmed, Hassona D (2014) Corporate Goverance and Firm Performance. Unpublished Master Thesis Faculty Of Postgraduate Studies And Scientific Research German University In Cairo.

-

Naveed A, Shoukat M, Muhammad N, Hamad N (2014) Impact of working Capital on Corporate Performance: A Case Study from Cement, Chemical and Engineering Sectors of Pakistan. Arabian Journal of Business and Management Review 3(7): 12-22.

-

Tamimi A, Fuad R, Qaisi A, Faris A (2012) The Impact of Internal Corporate Governance Tools on Working Capital Management and Their Impact on Economic Addition: An Applied Study on a Sample of Industrial Companies Listed on the Amman Stock Exchange, The Eleventh Annual Scientific Conference ( Business Intelligence and the Knowledge Economy), Al-Zaytoonah University of Jordan.

-

Guide to Corporate Governance Rules and Standards in the Arab Republic of Egypt issued in 2011. Alim A, Ahmed A, Senussi A, Zaazoua H, Salih MM (2016) Principles of Financial Management. Dar Al-Nahda Al-Arabiya.

-

OCED (2004) Organization for Economic Cooperation and Development Principles.

-

Mona Ali M (2014) Study of the relationship between internal governance mechanisms and the capital structure. Unpublished master’s thesis, Cairo University.

-

Wajih NA, Hafeez A (2013) The Impact of Applying Corporate Governance Mechanisms on Information Content in the Stock Market: An Applied Study. The Scientific Journal of Economics and Trade. 1: 467-493.

-

Abdelmegeid NS (2014) Impact of corporate governance on working capital management and financial performance. The Thought Accounting 19(1): 35-71.

-

Al-Fayoumia NA, Abuzayed BM (2009) Ownership structure and corporate financing. Applied Financial Economics pp: 1-10.

-

Al-Haddad W, Alzurqan ST, Al-Sufy FJ (2011) The Effect of Corporate Governance on the Performance of Jordanian Industrial Companies: An Empirical Study on Amman Stock Exchange. International Journal of Humanities and Social Science 1(4): 55-69.

-

Agyei A, Owsus A (2014) The Effect of Ownership Structure and Corporate Governance on Capital Structure of Ghanaian Listed Manufacturing Companies. International Journal of Academic Research in Accounting, Finance and Management Sciences 4(1): 109-118.

-

Aljifri K, Moustafa M (2007) The Impact of Corporate Governance Mechanisms on the Performance of UAE Firms: An Empirical Analysis. Journal of Economic & Administrative Sciences 23(2): 1-4.

-

Basheer MF (2014) Impact of Corporate Governance on Corporate Cash Holdings: An empirical study of firms in manufacturing industry of Pakistan. International Journal of Innovation and Applied Studies 7(4): 1371- 1383.

-

Carter DA, D’Souza F, Simkins BJ, Simpson WG (2010) The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review 18(5): 396-414.

-

Amarjit G, Nahum B, Mand HS, Charul S (2012) Corporate Governance and Capital Structure of Small Business Service Firms in India. International Journal of Economics and Finance 4(8): 1-8.

-

Gill A, Shah C (2012) Determinants of corporate cash holding s: evidence from Canada. International Journal of Economics and Finance 4(1): 70-79.

-

Hasan A, Butt SA (2009) Impact of ownership structure and corporate governance on capital structure of Pakistani listed companies. International Journal of Business & Management 4(2): 50-57.

-

Heng TB, Shabnam A, San OT (2012) Board of Directors and Capital Structure: Evidence from Leading Malaysian Companies. Asian Social Science 8(3): 1-8.

-

Kamardin H, Haron H (2011) Internal corporate governance and board performance in monitoring roles: Evidence from Malaysia. Journal of Financial Reporting & Accounting 9(2): 119-140.

-

Lückerath Rovers M (2013) Women on boards and firm performance. Journal of Management & Governance 17(2): 491-509.

-

Mulyadi M, Anwar Y (2015) Corporate Governance, Earnings Management and Tax Management”, Procedia - Social and Behavioral Sciences pp: 363-36.

-

Christopher P (2004) Corporate governance and the role of non-executive directors in large UK companies: an empirical Study. Corporate Governance ProQuest pp: 1-12.

-

Ramly Z, Abdul Rashid HM (2010) Critical review of literature on corporate governance and the cost of capital: The value creation perspective. African Journal of Business Management 4(11): 2198-2204.

-

Rantiu A (2013) The Effects Of Board Size And Ceo Duality On Firms’ Capital Structure: A Study Of Selected Listed Firms In Nigeria. Asian Economic And Financial Review 3(8): 1033-1043.

-

Rezaei F, Ghorbani B, Yaghoubi A, (2012) The effect of corporate governance on enterprises’ finance structure. Journal of Contemporary Research in Business pp: 1-15.

-

Mohd SN (2010) Corporate Governance Compliance and the Effects to Capital Structure in Malaysia. International Journal of Economics and Finance pp: 1-10.

-

Shleifer A, Vishny RW (1997) A survey of corporate governance. The Journal of Finance 52(2): 737-783.

-

Sheikh NA, Wang Z (2012) Managerial Ownership and Earnings Management: Theory and Empirical Evidence from Japan. Journal of International Financial Management & Accounting 19(2): 1-15.

-

Vasile E, Croitoru I (2013) Corporate governance in the current crisis. Internal Auditing & Risk Management pp: 1-12.

-

Velnampy G (2013) Corporate Governance and Firm Performance: A Study of Sri Lankan Manufacturing Companies. Journal of Economics and Sustainable Development 4(3): 228-236.

-

Wilson N, Wright M, Scholes L (2013) Family business survival and the role of boards. Entrepreneurship Theory and Practice 37(6): 1369-1389.

- Capacity Constraints in Pediatric Inpatient Psychiatric Care: A Cross-Sectional Analysis of Bed Availability and Geographic Access in North Carolina

- Why Healthcare Analytics Still Optimizes the Wrong Things

- Coding, Coverage, and Care: The Infrastructure of Transgender Health Inequities

- The Effect of Classroom Attendance on Academic Achievement of Management and Leadership Discipline of Nursing Students at Instituto Superior Cristal and Universidade de Dili, Timor-Leste, 2024: A Case Study

- The Role of Social Bonds in Facilitating Shared Investments and Resource Allocation: Addressing the “Wrong Pocket Problem” in Public Health and Healthcare

- Social-Cultural Factors Contributing to Antimicrobial Resistance in Livestock Farmers and Community Households in Kayonza District, Rwanda