Covid 19-India: Enigma of Saving Lives or Economy

Introduction: The entire world is assuming that it is fighting a war against Covid 19. After more than six months since the world first heard of the novel Corona virus, we still do not know many things about it. This pandemic will amplify existing social fractures and inequalities. Purpose: The purpose of this paper is to highlight the economic impact of the pandemic due to rising joblessness and shrinking economies, investments in building infrastructure and cost of care in hospitals and subsistence to the poor and labourers etc Design: This is a review of Covid 19 pandemic its impact on health and economic of India Findings: The immediate impact of the COVID-19 virus- fear, illness, and death are explicit. Indirect health effects like more people dying of other chronic morbidities due to poor access to services during lockdowns and denying of non-emergency care for over 6 months. Most importantly people are losing trust in healthcare system. The issue of political consequenceshow world powerful countries choose to look after themselves versus the rest of the world that will define global politics over the coming decades. As some governments face perceived or actual failure to protect their citizens, leading to blame others. The issue of the social and economic impact due to rising joblessness and shrinking economies, investments in building infrastructure and cost of care in hospitals and subsistence to the poor and labourers is yet to be realized fully. The economic consequences of the pandemic may well be more significant for India than the epidemiological impact compared to any other large developing country. Conclusion: A valuable debate about whether India has the fiscal room to afford a substantial stimulus that is taking place. it is important to note that the size of India’s support program is by far the lowest, as a percentage of GDP, among the top 10 global economies. If policymakers make it abundantly clear that unconventional policies will be time- and event-specific and would be unwound once its objectives are achieved, the financial macro stability will not be affected. On the brighter side, investors should start focusing on a targeted fiscal package to be able to contain the immediate downside. Materials & Methods: Data Collection Methodology: This paper used the data from WHO dashboard, Ministry of Health & Family Welfare, GOI India or States National Health Mission websites or other websites, WHO dashboard or other websites like John Hopkins’s University, CDC Atlanta, NSSO, Google and Wikipedia etc. I have also used the data as reported in daily new papers, mainly Times of India, Bangalore, Delhi and Mumbai editions and other national English dailies and regional vernacular print media in southern states. Study Setting & Sampling: The review covers entire country by major states and cities setting. Being the secondary data review no sampling was done

Introduction

On 15th July 2020 at 0920 CEST there were we have 13,495,260 Cases of which 7,881,023 recovered and 582,125 died and the rest are active. Covid 19 infections globally [1]. While USA contributes 3,344,738, Brazil 1,884,967 and India reported 936,781, cases. In India, the disease began late, initially spread slowly due to lockdown but has now started increasing amazingly fast and the spread continues, Out of 208,087 new infections reported in last 24 hours while USA had a share of 58,720 compared to 29.429 in India in last 24 hours. Total number of cases per million population in descending order work out to be, in Belgium 843.3, UK- 651.7, Spain-607.7, Sweden- 538, France-458.4, USA 394.7 and in India only 14.2 as against World Average of 69 (Figure 1).

On 30 January 2020, the first case of the COVID-19 was confirmed in Kerala, India that originated from China. Soon it spread across the country and as on 15th July 2020, Indian cumulative figure reached close to a million (968,835) cases and cumulative toll of 24,860 [2]. The first fifteen days of July reported 383,361 cases and 7,468 deaths compared to 400,413 cases and 11,988 deaths for the entire month of June 2020 and record 32498 cases and 615 deaths in the last 24 hours, indicating the surge in the cases and deaths is a worrying signal [3]. The most worrying fact is the pace at which the cases are being increasing in the recent days. While first 100 000 cases took 107days in India the recent increase from 800,000 to 900,00 and to the 100,000 taking just 4 days [4]. Despite limited testing the increase in numbers, that too symptomatic cases are not as alarming as in countries like USA, Italy, UK etc. The daily increase numbers touched 34,000+ (+14%) an increase of more than 4143+ cases in last 24 hours on 15 July 2020.

The case load works out to be 4657 per million populations in India. Deaths per million is rising week after. Compared to a figure of 300 per million populations that some of the European countries have reached, the above-250/million figure that the United States has reached, or above-four figure that some of the Asian countries have reached, India is 15 per million populations a rate far below many other countries. Amongst active cases requiring critical care in India, only 0.45% needed a ventilator, 2.94% needed intensive care and 2.94% need oxygen support that means only 6.3% of active cases required critical care. An average gap between the actual occurrence of symptoms and death is 10-15 days and deaths today are telling us what the situation was about 10-15 days back in terms of infections. Most Public health Professional in India believe that deaths per day are the best indicator for us to find out whether we are getting control over the epidemic or not. looking at the number of new tests performed each day, and the number of new cases detected from those, as a fraction, and it is coming down trend will be another way of looking at the progress of the pandemic.

Results

Pandemic

After more than six months since the world first heard of the novel Corona virus, we still do not know many things about it. The world has not been able to freeze even the presenting signs and symptoms. Initial list of symptoms consisted of throaty pain, cough, fever, breathlessness, now includes loss of smell, appetite, skin rashes, eye infection, diarrhoea, happy hypoxia and even viral carditis [5]. Severe backache, abdominal pain, aching calves could also be the calling card of the virus. More recently neurological signs like Encephalopathy, Encephalitis and Guillain-Barre syndrome are being associated. Recent studies in Gujarat it has been observed that the well-known risk of clotting of blood vessels prolongs for weeks in some patients an important complication. This makes recovered patients susceptible for heart attacks, brain strokes and pulmonary embolism leading to sudden deaths. Persistent Hiccups as atypical presentation of COVID is the recent symptom added (www. researchgate.net › publication 19 June 2020) [4].

The mode of transmission was initially assumed as droplet infections that could be controlled by frequent hand washing, avoiding touching face, eyes, cough etiquette, physical distancing and wearing mask. Now with the understanding of other modes of transmission like GI route, airborne etc. the world is still in learning curve. The worst is we are unable to assess how many have been infected. Reverse Transcription-Polymerase Chain Reaction (RT-PCR) is the gold standard frontline test for coronavirus (COVID-19) and that rapid antibody test cannot replace it. The confirmatory test (PCR) demands up gradation or establishment of laboratories at each district level in India. WHO guidelines emphasise the need for comprehensive testing (testing 140 people per day per Million populations at risk). India is conducting around 201 tests per day per million populations very recently. Around 22 states in India are conducting at least 140 Covid-19 tests per day per million populations as of 14th July 2020. The proportion of RT-PCR: Rapid tests are in the range of 30-40%: 70-60%. Test Positivity rates (TPR) of the two types of tests are in the range of 35-40%: 5-7% respectively [4]. Among the states with high disease burden, Delhi’s testing rate is the highest at 978 tests per day per million population, whereas Tamil Nadu is doing 563. Maharashtra is conducting 198 tests per day per million population. Gujarat and West Bengal were among the states with testing rate below the 140 mark [5]. Testing will ensure early detection and treatment to reduce mortality due to the viral infection. At present, there are 1,206 labs across the country equipped to conduct Covid-19 tests and on 13th July 2020 India conducted 2,86,247 tests, taking the total tests done in the country so far to 1,20,92,5034. The Rapid Antibody Test gives us an idea about prevalence of disease in an area and thus is used for epidemiological studies and surveillance purpose in hotspots. Rapid Test kits are not fully accurate, they give 15-20% false negative results and most importantly RAT kits need to be imported.

The total number of confirmed coronavirus cases globally reached 13,462,461 on Wednesday, the 15th July 2020 according to World meter. Today, we know that the US, with over 3.5 million cases, is the most affected country. It is also the country that has conducted the greatest number of tests after China, where the virus was first reported. The US has so far conducted 132,993 tests per 1 million of its population. By comparison, India, which has a population over four times as big as the US’, has conducted just 8,991 tests per 1 million people. India is the third worst-hit country with 936,181 coronavirus cases as on 15th July 2020.

Many country’s health agencies estimate that the number of infections is more than ten times of the official tally in each country. We are still trying to understand how the infection attacks human body, how our immune system responds, what are the pathological changes and why there is differential in attack rate by age, socio-economic status, virulence, rates of hospital admissions, and need for oxygen or ventilators. All these decide how the economic gets affected in the process of management. Recently it has been seen among China patients that the immunity lasts for just 2-3 months and re-attacks are not uncommon. It is just not the antibodies that fight the viruses. It may also be immune system cells designed to repel the virus while the people have been infected also producing memory cells that can rapidly churn out antibodies if the virus invades. A study conducted in King’s College London found an increase in P10 molecules which is responsible for sending T cells of the body where are they are needed in Covid patients. Ordinarily they are elevated only for brief period but in Covid-19 IP10 levels go up and sustain at high level for long. This may be a reason for confused response from immune system. Biopharmaceuticals company Biocon has secured approval from the Drugs Controller General of India (DCGI) for its plaque psoriasis drug Itolizumab (ALZUMAb) for emergency use in Covid-19 patients. The approval is for 25mg / 5ml injection solution of the medicine to treat cytokine release syndrome (CRS) in moderate to severe acute respiratory distress syndrome (ARDS) patients with Covid-19. It is the first new biologic therapy approved globally for the treatment of moderate to severe Covid-19 complications. The drug is an anti-CD6 IgG1 monoclonal antibody introduced in India in 2013 under the brand name ALZUMAb to treat chronic plaque psoriasis. Biocon repurposed the drug for the treatment of CRS associated with Covid-19. Itolizumab acts via immunomodulation. It binds to the CD6 receptor and blocks the activation of T lymphocytes, in turn suppressing the pro-inflammatory cytokines and decreasing the cytokine storm and inflammatory response. Many countries are putting all out efforts to produce vaccines against Covid 19 that may take from 6-18 months to be available in the market.

Economy

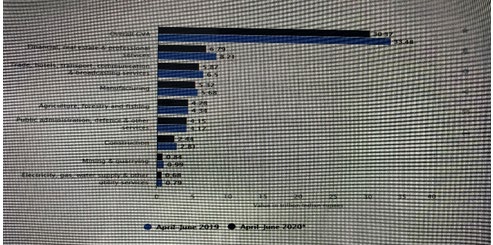

Global reality is world economies are tanking due to outbreak of Covid19. Things cannot be investigated in isolation. It is relative context and bounce back in post-Covid scenario that matters the most. The state of the economy at this point is difficult to explain. While estimating the cost of Coronavirus on the economy, one needs to look at the gross value added, (GVA) which is a measure of the total value of goods and services produced in the economy without accounting for taxes and subsidies (Figure 2). The GVA growth rate in April-June 2020 declined in a range of -4.6% to -8.8 % compared to 2019-20, according to a forecast the study [6].

The National Statistical Organisation (NSO) on 13th July 2020 reported that the Inflation as measured by the consumer price index (CPI) rose an annual 6.1% (Rural 6.2 and Urban 5.8) in June, higher than the 5.8% in March 2020 [7]. With China’s economic growth predicted to drop at least from 6.1 to 5.6 percent because of the coronavirus, Indian economies will be affected worse than China. India must consider their economic responses as well as their health safeguards. “The Covid-19 pandemic, which started as a public health crisis, has led to significant disruption in economic activity, mainly due to the measures taken to limit the spread of the disease. It has affected not just health but all sectors of the economy, including but not limited to manufacturing, aviation, tourism, transportation, construction services, agriculture and others,”. Private and informal retail businesses and the economy have suffered massive losses. The unlock down and financial support by Governments since last month had enthused Mini, Small and Medium (MSME) Industries production house to start production activities.

India imposed hardest nationwide lockdown in the world since 24th March 2020. Government of India offered a mix of monetary and fiscal measures. The five- part announcement of stimulus of about 267,000 million US$, in Mid-May 2020 by Government of India aimed to tide over the immediate challenges caused by the lockdown was a welcome step. The structural reforms required to make India more competitive economy are yet to be rolled out. Just 40 years ago India was in level with China today’s second largest economy in the world in terms of income, life expectations transport system etc. While China’s Deng reforms in 1980’s helped it surge past us in all most all socio-economic parameters. The Covid 19 pandemic stuck them early and they already are in reviving their economy, whereas in India we are yet see our peak of epidemic, in lock downs, struggling to be self- sufficient to establish laboratories, produce rapid testing kits, ventilators, PPEs gloves etc that have disturbed all most all other productive and economic activities.

Discussion

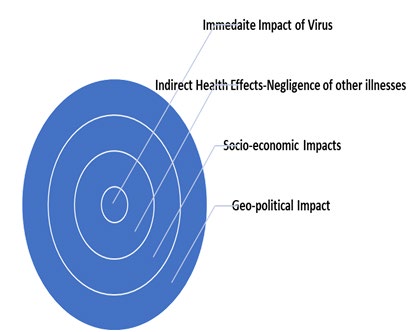

To understand the Covid 19 crisis fully, it may be useful to imagine the concentric ripples generated by Covid 19 in the Global pond [8] (Figure 3).

- The innermost circle is the immediate impact of the virus: fear, illness, depression, and other mental illnesses due to stigmatization and death.

- The second, larger circle describes COVID-19’s indirect health effects, such as more people may die of malaria, Cancers, CVDs, Diabetes, COPDs, Urinary system illnesses due to poor accessibility of health services during lockdown and competing priority of hospital beds and other services for Covid 19 patients and also as missed opportunities for screenings, detection and management of cancers, diabetes, hypertension, endocrinal disorders etc. And most importantly people losing trust that can take years to regain trust in healthcare systems.

- The third circle, the social and economic impact of rising joblessness and shrinking economies, investments in building infrastructure and cost of care in hospitals. This pandemic will amplify existing social fractures and inequalities. This will have political consequences. Some governments may fall because of COVID-19 mismanagement and loss of faith of the people of such countries.

- The biggest circle- geopolitics. How world powers choose to look after themselves versus the rest of the world will define global politics over the coming decades. As some governments come to face rising criticism for their perceived or actual failure to protect their citizens, one natural response will be to blame others [8].

Saving Health of the Population

After more than six months since the world first heard of the novel Corona virus, we still do not know many things about it.

We understand that the disease is not so virulent as only 4.6 % of cases died and if you consider the competed case fatality rate is around 7.32%. There are at least 3-4 infectious disease like Tuberculosis, Cholera, Malaria and HIV AIDS, that have much higher CFRS & CCFRs.

The treatment protocols are also being upgraded. The severe morbidity and deaths were mainly due to hyper- inflammation and hyper-clotting especially in lungs as main complications. The recent observational studies in Gujarat and Mumbai hospitals indicate that the risk of clotting in some patients prolongs weeks after they recover. This makes recovered patients susceptible to sudden heart attacks, brain strokes and pulmonary embolism [4]. Checking such patients D-Dimer levels periodically and continuing anti-thrombosis medications for extended periods are being recommended.

As business reopen and activities resume one major consideration is determining when it is safe to send children to schools. As of today, children and adults up to 20 years in India from about 14% of cases and just 2.1% of deaths. However, in the recent weeks the infection among under 20 years has gone up, as Karnataka the home state of the author has witnessed a 261% increase in children below the age of 10 years testing positive for Covid-19 in June alone. While that is worrying enough, worst worry is most of these children do not have travel history. On June 1, there were 298 infected children in the up to 10 years age group and by July 1, the number had touched 1,076. Of the infected children, 423 are below the age of five. As on July 1, these children accounted for 6.5% of the total (16,514) infected in the state. Paediatricians and Public Health experts feel that the children confined to their homes may have been infected by elders, especially parents. In many cases, the parents were negative. The children can spread the disease as they have same or greater viral load and due to their meeting other many more time than adults in schools and playgrounds [4, 8, 9].

Saving Economy

New global reality is world economies will be tanking due to outbreak of Covid19. The bounce back which matters restricting only to an Indian context will be a fake narrative. Things cannot be investigated isolation it is relative context and bounce back in post-Covid scenario which matters the most. Optimism, if any, about the state of the economy at this point is difficult to explain. There is little ammo left with the governments even among most developed and financially sound countries after the reforms they tried to execute in the recent past did not exactly restart the economic engine (Chart 1).

Chart 1: The Routes of Economic Impact of Covid 19.

The decline in India’s fortunes had started quite a while ago; the virus struck an economy with pre-existing conditions. May be PM and some Ministers are not corrupt but situation at ground level whether you want land water or power anything for that matter without greasing palms right from lowest level can you get it because they are conduits. What can you get from such Governments Centre or States? The GOI did not anticipate the effects of its actions on three occasions; a) the first was when the Note Ban that affected many industries had to shut shop and lot of people lost their jobs. The government had no plan how to deal with such a situation. B) The second one was hasty introduction of GST. The technical glitches are persisting and filing of GST is not an easy process even today. The government has not been able to solve this issue satisfactorily. C) The third one is migrant workers’ plight when lock down was imposed. The sudden large scale exodus of migrant workers escalated the Covid-19 spread as proper arrangements for their transport had not been thought of. Added to these the hurdles in starting business-like return of labours from their home villages, financing Micro, Small and Medium Industries (SMEs) in India even today is making the foreign investors to hesitate to invest and start their business in India [10]. The economy was doing rather good in 2016-17. The GST they said was a revolutionary move. It would subsume 17 other taxes and simplify taxation. It did. The rates however were so unreasonably high that it killed demand. People found that tax was higher than the profit in making and selling items. Then came the ill-conceived MV act that tweaked mandatory requirements for autos [11, 12, 13, 14].

The major sources of revenue in India are- in-country and international travel that is hurt badly due to banning of all transport systems (Rail, Air. Taxi and Bus route) exercise revenue, tourism, education system. Starting from institutions such as Indian Institutes of Management and Indian School of Business to all private schools have started the pinch of the Covid-19 disruptions as companies cannot collect fees have to plan to slash their training budgets for top business schools. Resorting to digital teaching methods have increased the cost both to the institutions and families. The Covid-19 pandemic has led to further significant disruption in economic activity, mainly due to the measures taken to limit the spread of the disease. It has affected not just health industry but all sectors of the economy, not limited to manufacturing, aviation, transportation, tourism, construction services, agriculture, and others. Private and informal retail businesses and the economy have suffered massive losses. Even the high-cost longer duration programmes for working professionals, could come under pressure in the next 12-24 months as the pandemic-hit economy and rising joblessness are forcing professionals and corporates to tighten their purse strings [15].

According to a study Titled ‘Impact of Covid-19 Pandemic on Labour Supply and Gross Value Added in India’ published as a working paper by the Indira Gandhi Institute of Development Research (IGIDR) [9], India lost Rs 33,800 crore in wage loss caused by job cutbacks in the country in the first two lockdowns alone. The first two lockdowns, from March 25 to May 3, resulted in 19.5 crore workers facing the risk of job loss. These workers remain jobless for a continuous six months, at least the total expected wage loss would amount to Rs 2 lakh crore. Most workers who were at risk of job loss in the first two lockdowns were from states with the highest number of Covid infections like Maharashtra, Delhi, and Rajasthan. Also, 70% of workers at risk of job loss will be from the top 10 states. Given the fact that most labourers in these sates have migrated back to home villages the labour supply disruptions would persist, and more workers would be rendered jobless. Informal workers are the worst affected. Workers in urban parts have been more affected than rural because curbs were fewer, with the bulk of activities in rural parts classified as essential. It is estimated that In Lockdowns so far 72% of the workers in the urban parts of the country and 26% of the workers in the rural parts lost their jobs4. “The most impacted sectors in Lockdowns so far were wholesale trade, constructions, the hotel industry, transport, retailers, manufacturing, and the entertainment sector, including malls and movie theatres [9]. A global survey for the second quarter of 2020 by Global Economic Conditions survey by Association of Chartered Accounts (ACCA) and Institute of Management Accounts (IMA) for Q2 2020 with accounts and Chief Financial officers suggests that India is heading for further economic contraction this year as pandemic mitigation measures have hurt domestic demand and the global recession has impacted the exports.

Impact on Key Financial Sector

a. Merger & Acquisition Activity: Most Indian states are battling with the spread of the virus in which various mobility restrictions mechanisms are adopted: ranging from enforcement of quarantine, travel ban, curfew to total lockdown, As such, these events could potentially be significant enough to trigger a change to the terms of an M&A transaction currently in progress, transaction deals could be delayed. The pandemic situations could also cause setback to M&A due sedulity and carefulness, necessary for a transaction to progress to finalization which eventually could result in the termination of the deals. While on one side this could hamper investment opportunities and consumers demand in Indian states, on the other hand we have an opportunity of USA and European country investments moving out of China and for them India appears to be attractive and big market. Restriction of China products and scrutiny of China’s investment may hurt Indian production activities as we depend upon China for many raw pharmaceutical and automobile materials and IT equipment. Recently launched self-Reliance “Atma Nirbhar program” may pose take off challenges in many MSME sectors at least for short time. b. Insolvency Process: Lenders who have put on sale assets worth thousands of crores under the insolvency process are finding it difficult to complete deals because of the lockdown. Banks have been trying to sell several companies like DHFL, Jet Airways and SevenHills Hospital, long before the Covid-19 pandemic broke out and had even received bids. But in these transactions, firm bids are still awaited. Completing resolution in the sale of Jet Airways, DHFL and Seven Hills Hospital has also got delayed. The handful of transactions that have taken place are those that have been in the pipeline where the bidders have had a chance to complete the due diligence before Covid-19 in the previous financial year. Bidders are reluctant to put in a firm bid as physical visits and informal talks with the management are not happening. As a result, lenders have kept putting off the last date for sale of companies. Also, bidders who put in expressions of interest are having a rethink on the valuation, given the economic crisis caused by the pandemic. The key problem is the inability to do a physical inspection. As “Physical visits and meetings with management give an idea about the real situation on the ground. c. Financial Institutions: The activities and responsibilities of the Indian financial institutions might be shelved because of the scepticism and doubt surrounding the impact of COVID-19, there is decline in the confidence of financial investors and stakeholders. It remains unclear whether the huge global economic downturn caused by decreased output in China will impact on Indian lenders and compel financial institutions on the continent to be more lenient towards borrowers and cut them some slack. Indian stock market Sensex has gained 40% since hitting a low of 25,981 on March 23. Markets have climbed since June 1, and reached a level of 36,594 even as the number of daily new Covid-19 cases rose from around 9,000 in the first week of June to over 26,500 on 10th July 2020 [4]. d. Local Markets: Since commodity prices determines the rate of State-specific economic growth. Local prices of have been driven down by the virus’s global impact. The uncertainty of the impact of COVID-19 on local markets is expected to lead to increased risk aversion from investors who are waiting to see its potential impact in respective states. Because of the restricted movement of the population the doorstep delivery services have added extra costs adding burden to middle class population. On advantage, a partial drop in the cheap labour and restricted movement of local products, has increased the availability locally and drop in prices provides opportunities for smart investors. e. Insurance: Most health insurance policies require that a patient be admitted to a hospital for at least 24 hours for the insurer to cover the bill. However, since many Covid-19 patients with mild symptoms are being encouraged to stay home, the requirement for hospitalisation is set to go. At least one general insurance company rolled out home healthcare benefits recently, allowing customers to get treated at their residence for any ailments. Some insurers have started covering home healthcare on a case-to-case basis. More are likely to follow suit. Healthcare experts see this as a game- changer that will not only prompt more people to opt for these services but also reduce the burden on hospitals. After the insurance regulator, the Insurance Regulatory and Development Authority (IRDAI), noticed that the Covid-19 claims, at around 8,500, paid out by insurance companies were disproportionately lower than the number of Covid cases in the country, it came up with two standardised policies which all non-life and health insurance companies have been told to mandatorily offer from July 10-a) Emergency covers: Before the pandemic, life insurance companies could sell only long-term policies, but the regulator has now directed life and non- life insurers to introduce short-term Covid-19 health covers for a period of 3 to 11 months. This was done to make such policies more affordable for those who do not have any health insurance cover or cannot afford it. While some of these changes may be specific to the Covid-19 pandemic, the insurance industry’s experience with these changes will determine if they become the new normal too b) Pandemic Risk Pool: As Covid 19 is an emerging disease , has not been captured in any existing insurance contract. In India, Businesses, properties, and individuals would usually not be covered in insurance policies, irrespective of whether the insurance covers business interruption, damage to properties, product loss of life and products or travel insurance. With the coronavirus pandemic causing massive disruption and losses across sectors, the Insurance Regulatory and Development Authority (IRDAI) has proposed creating a “pandemic risk pool”. The aim is to provide cover to risks related to the virus. A pool refers to the practice of insurance companies coming together and committing funds to meet claims arising out of any insured risk in proportion to the business they do. In this manner, claim pay-out is equally shared among all pool participants. This method is followed when there is too much uncertainty about the risk for any insurer to take a call, like in nuclear risks, or when the losses are high and companies are reluctant to issue policies, as in motor third-party insurance.

f. Excise In the first unlock period the early trends of long queues outside shops gave an impression that the alcohol industry would remain an outlier in a moribund economy. But unrealistic’ tax on alcohol has done more damage to the industry than the pandemic. Demand in states has tumbled, with brewers bearing a major brunt. “After the drastic price hike in some states, the industry has registered about 80 per cent decline as compared to previous year in overall beer volume in May - a peak season for beer. The hike in duty is also having knock-on effects on the ancillary segments as well, especially farmers, the entire supply chain ecosystem with barley malt suppliers and logistics partners. In India, beer is taxed 60 per cent higher than stronger spirits despite the lower alcohol content, that ranges from 4-7 per cent as against upwards of 40 per cent in hard liquor. With the disparity in taxation, the prices have increased. For example, a bottle with MRP of Rs 100 earlier, now sells at Rs 170. Such a “short-sighted approach” that would subsequently engender a loss in state revenues and force consumers to opt for cheaper, low-quality drinks to avoid burning a hole in their pocket, that could affect their health adversely. So far, the overall price has increased in 18 states and the hike in taxes ranges from 10 per cent to almost 75 per cent. While volumes were impacted across categories in the months of May and June 2020, the premium imported liquor brands will be the hardest hit if bars remain shut. The revenue from alcohol as the percentage of states’ own tax revenue at about 21 per cent and as the percentage of revenue receipt is about 10 per cent, or Rs 2.25 lakh crore. Confederation of Indian Alcoholic Beverage Companies (CIABC) has sought for a “realistic” corona cess on alcoholic beverages. As Differential rates of taxes in different states are applied CIABC has warned that the has porous borders and liquor prices in neighbouring states are much lower which is creating unlawful smuggling and depriving the state of its tax revenue [4].

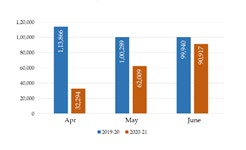

g. GST The collection of Goods and Services Tax (GST) for June 2020 has seen a downfall as compared to that in June 2019. The GST collected for June, amounted to ₹ 90,917 crore (CGST- ₹ 18,980 crore SGST- ₹ 23,970 crore IGST- ₹ 40,302 crore Cess- ₹ 7,665 crore) the departments have already settled ₹ 13,325 crore to CGST and ₹ 11,117 crore to SGST from IGST collections. The total revenue of the State and the Central government is ₹ 32,305 crore for the CGST and ₹ 35,087 crore for the SGST. Due to the countrywide lockdown stemming from the coronavirus pandemic, a lot of return filing was pending, and revenue collections have been depressed. In addition, GOI has decided not to levy any late fees for all those who have no tax liabilities but who have not filed their returns between July 2017 to January 2020 (Figure 4). Even if there is a tax liability, the maximum late fee will be capped at Rs 500 per return. The reduced rate of late fee will apply for all the GSTR-3B returns furnished between July 1 to September 30 this year [15].

Impact on Infrastructure

India sources from China electrical equipment and machinery, mechanical appliances, semi-conductor devices, fertilisers, iron and steel products, coal, auto components, textile fabric, project goods and accessories, and antibiotics. Recent bids are viable only based on Chinese imports, as modules manufactured in India are far more expensive.” A move to curb imports in under-construction solar projects can be expected to lead to tariff revisions. Import curbs here also entail risks of project delays. The Indian agrochemical industry imports a high amount of raw materials from China. The companies with generic product portfolios have higher dependency for raw material from China.

On the flip side, some domestic capital goods firms may potentially benefit from the re-look at ties with China. Joint venture (JV) with Chinese players in the past five years won $1 billion rail projects due to technical expertise and a means to reduce competition through partnership. Incrementally, $10 billion-plus tenders are in the pipeline in metro rails in different states.” If bidding is restricted for Chinese companies for larger projects, Indian companies may well benefit. In the long-term, tensions between both nations would give a push to the “Atma Nirbhar” a Make in India initiative. This would help India become self-reliant and create more employment opportunities., though as raw material dependency is challenging to overcome. some states are naturally blessed, India can go a long way in making value-added products [1].

Impact on Trade

COVID-19 pandemic is speculated to affect China’s – India trade for several months. Indian industry’s dependence on these imports is organic and has developed over years and decades. India’s supply chains are critically reliant on these imports. China is certainly not the sole source of these products, but it is the leading source. For example, India is dependent on China for compressors, which forms 30-35% of the total cost of air conditioners, and very few consumer durables firms have meaningful in-house manufacturing capabilities. Similarly, Indian drug makers are heavily dependent on China for active pharmaceutical ingredients (APIs). The Indian consumer durables sector has close linkages with China. The recent India-China border tensions intensifications is adding fuel to fire in some key sectors. “Indian drug makers import about 70% of API requirement from China with imports from the country increasing steadily over the years (from about 62% in FY12 to about 68% in FY19).” Chinese API manufacturers have an advantage over India in terms of cost competitiveness, thanks to their scale benefits. Import ban on Chinese pharma-related products may lead to supply-chain disruptions for Indian firms [13]. This, in turn, may mean adverse price movements, increasing costs for domestic firms. China caters to a majority of smartphone demand in India and even globally. Therefore, any disruptions will result in a spike in smartphone prices and probably lead to a delay in the adoption of new technologies such as 5G. India imports a vast portion of its solar modules from China. In practice, complete self-reliance is not even a practical objective for any country as no country can produce everything it consumes. A better option is to build an efficient, globally competitive economy. Our size will then ensure that we have economic bargaining power. Perhaps we should also develop alternative sources of supply of crucial inputs to insure against any external blackmail [13].

Impact on Energy and Mining

Indian mining and Energy industry face an inevitable hit from COVID-19 outbreak. The mining sector in India was poised for robust growth in FY21, on the back of rising demand from end-use sectors and fresh investments announced by the mining companies. Even though in most states mining was allowed even during the lockdown the effects have nonetheless been felt and may continue in the near term as the lockdown is extended. Demand in the end- use industries like power, steel, cement, aluminium, etc. has come down. Simultaneously transport and logistics are affected, limiting offtake of minerals from the mines. The consequential effects of reduction in activity in the mining sector have been: a) Government exchequers are expected to get affected as collection against statutory levies, b) taxes are lower due to lower volume of mineral production c) Government’s plan to auction new coal and mineral blocks is likely to get delayed and d) Lastly but not the least COVID-19 has already affected the entire business eco-system especially the marginal stakeholders like small vendors/contractors, contract labourers, downstream and ancillary businesses, etc.

Impact on Industrials, Manufacturing and Transportation

Due to Covid 19 pandemic construction companies is currently affected due to the fallout of shortage of raw materials, skilled personnel who are unable to travel for project supervisions from the affected regions, and contractors are unable to secure projects due to travel restrictions and self-isolations. 50% + of India’s (organized long haul) trucking fleet is stranded without drivers, Local (short haul) transport, though less impacted, is working with reduced capacities. Trucks (including those carrying essentials) are still stuck for reasons including want of labour to load/ unload check-posts etc. Railways are stepping up and can serve a few sectors, but the gap is large, with first mile and last mile being a challenge. It is not clear as to when companies will commence production but once they reopen, both imports and exports will be further delayed by the aftermath congestion and backlog [16].

Impact on Healthcare and Pharmaceuticals

This Pandemic is currently putting pressure on health care system in in Indian states though each state is being vigilant to quickly test, diagnose, treat, trace contacts, and contain the viral outbreak. In Pharmaceutical sector, the prices of pharmaceutical products and drugs continue to rise or unavailable because of factory closures resulting in supply chain disruptions. During this crisis pharmaceutical companies are focusing on to respond, recover, and thrive [17]. India Pharma’s Global Standing: The Indian pharma industry has been a world leader in generics both globally and in domestic markets contributing significantly to the global demand for generics in terms of volume. Made-in- India drugs supplied to the developed economies such as the US, EU and Japan is known for their safety and quality. In recent years, India has seen increasing competition from China that has been able to leverage due to its inherent cost advantage. Risks from India Pharma’s China Linkages: India’s large import dependence on China (nearly 70% by value) has become a significant threat to India’s healthcare manufacturing and global supply chain. While Indian pharma players over a time period have steadily migrated up the value chain to focus on value-added formulations with higher margins, but this over dependence on China has increased the threat to the nation’s health security as some of these critical APIs are crucial to mitigate India’s growing disease burden. Supply Chain Disruption for India Pharma: Any disruption in supply chain of APIs can result in significant shortages in the supply of essential drugs in India. Some of the critical APIs for high-burden disease categories such as cardiovascular diseases, diabetes and tuberculosis are listed in the National List of Essential Medicines (NLEM). In fact, the current market is largely dependent on China for many antibiotic APIs manufactured by the fermentation route such as penicillin, cephalosporins and macrolides. India has significantly lost out on the API manufacturing owing to the inadequate government support and API infrastructure. Major earnings cuts ahead for pharma firms: Pharma as a sector has emerged as a strong contender to drive the next leg of rally, and therefore pharma stocks have seen a huge run up in the last 100 days. Relative stability, reasonable valuations: Indian pharma has been relative resilient to the Covid disruption and is poised to gain from favourable currency tailwinds and stable outlook for India and US business. The Key risks: a) extended lockdown can impact demand and manufacturing; b) Delay in US FDA plant resolution due to travel advisory; c) EM markets currency risks and subdued demand; d) delay in key approvals

Impact on Tourism and Hospitality

Many foreign nationals visit Indian states as students, tourists or as business travellers, now that this virus had spread across the country there were restrictions on non- essential travel events are banned, tourist centres are closed and mass gatherings are prohibited, the impact on the Indian tourism sector will be high. Hotels, airlines, luxury, and consumer goods have already recorded low patronage due to port closure of most Indian states and tourist attraction sites. Holiday visit to India have been cancelled and people have stopped going out to entertainment centres, stadiums, and kitchen cafe to avoid the risk of encountering the virus. In addition, the pandemic is seriously affecting Indian airlines, with a significant reduction in the number of flights to other countries from India.

Employment Status

India’s unemployment rate in June fell to 11% from 23.5% in May, according to data released by the Centre for Monitoring Indian Economy (CMIE) on 1 July 2020 as economic activities resumed after government eased pandemic lockdown restrictions [10]. Most well-known IT companies have Introduced an “extended bench period” where identified employees will be on loss of pay for three months. These employees will continue to receive their insurance coverage, but nothing else. The bench in IT companies is a reference to people who do not have billable projects to work on. That number tends to be 5-7% of total employees amounting to several thousand at any point, which is increasing to 12-15% since last few months [18].

Way Forwards to Minimize Covid-19’s Economic Impact in India

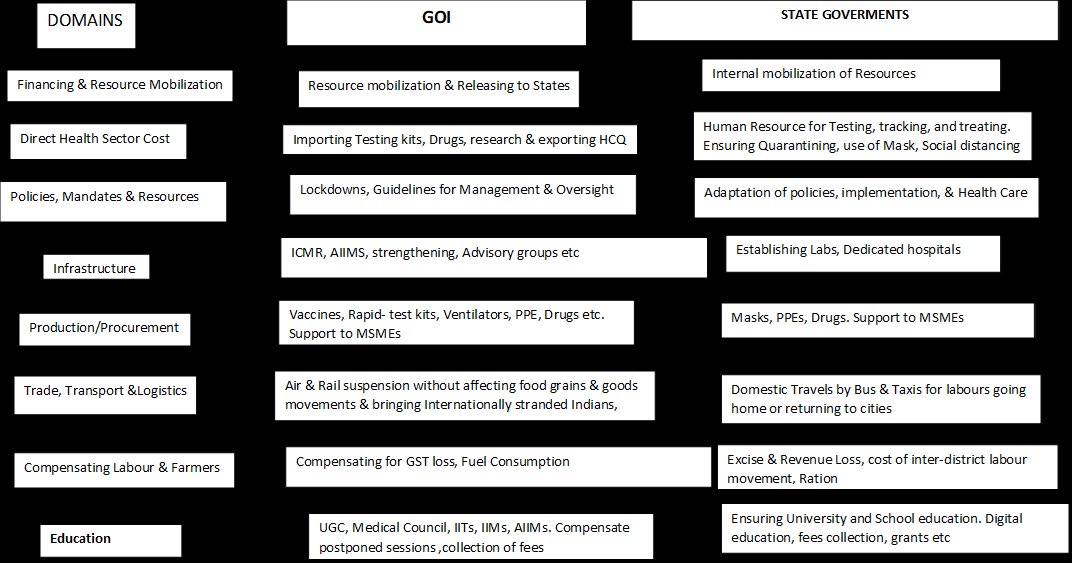

National (GOI) Efforts: The economic consequences of the outbreak may well be more significant for India than the epidemiological impact. With China’s economic growth predicted to drop at least from 6.1 to 5.6 percent because of the coronavirus, Indian economies will be affected worse than that. A turnaround strategy should include

- Response phase: Short-term (next 3 months or till the time the pandemic is contained): This phase will require the stakeholders to remain patient, and guard the ‘fundamentals’ with right policy directives from the Central and State Governments.

- Recovery phase: Medium-term (next 6 months to 1 year): Mid-term actions should target ‘recovery’ for setting realistic growth ambitions for FY22 by focusing on alternate options for mineral resource distribution and rationalisation of the tax structure. Companies can focus on optimizing their operating costs with adoption of digitalisation and technology enablement and focusing on value addition by diversifying into the larger part of the mine-to-mill value chain.

- Resilience phase: Long-term (next 1-2 years): Focus on creating downstream and ancillary ecosystem of business with the backward and forward interlinkages with other industry segments will must be driven State governments although it is unclear as to how much and for how long the sector will be impacted. Mining companies that provides lithium, copper and iron ore in India have already recorded reduction in demand from their partners in other European countries leading to global supply chain disruptions. The tendency of skilled technicians and contractors who to travel from affected areas and the capacity of labour- intensive mining operations to produce raw materials could be affected. India must consider their economic responses as well as their health safeguards.

Government of India Ministry of Health and family Welfare is importing test kits, preparing laboratory facilities, and working with states to support infection prevention and control and with airlines on traveller screening. Strengthening laboratory and institutional capacity in India has started yielding results in terms of improved laboratory diagnostics for this virus. Starting from a capacity of daily testing of 229 on 20 March 2020 it has reached over 200, 000 per day. There are now 1,223 testing labs in the country comprising 865 in the public sector and 358 private labs. Among the total 633 Labs are RT-PCR labs, 491 are TrueNat Labs and 99 are CBNAAT Labs The per day testing capacity is also fast growing, as over 2,00,000 samples have been tested on an average daily for the last 14 days, as of 15July 2020. “A cumulative total of 1,24,04,101 samples have been tested till 15th July with 325,000 samples being tested on July 14,”. Despite increase in sample size the positivity rate is stable around 10%. Introduction of Rapid antigen testing that constitutes 50% of the testing now and is the main reason for increased testing capacity. The consistent level of positivity may also mean that the testing is still high risk approach.

Studies have proven that air conditioning systems accelerate the spread of viral infections, especially the novel coronavirus since most air conditioning systems recycle the same air with very few air changes. The initial ‘experiment’, which has already commenced on the 15 pairs of trains that run on the Rajdhani routes, will soon be replicated on trains on other routes. It involves replacing the air intake in the Roof Mounted AC Package Unit (RMPU) system of Indian Railways AC coaches 16 to 18 times per hour — like what happens in OTs. Current air flow systems in the RMPU are designed to change the air 6 to 8 times per hour, resulting in 80% of the air being recirculate air with only 20% fresh air. OTs use 100% fresh air as chances of infection are extremely high. Alongside, the temperature settings for the air conditioning will be increased by 2 degrees Celsius, from 23 degrees Celsius to 25 degrees Celsius since passengers are no longer provided any linen or blankets. With all these changes the Indian Railways expect an increase of 10-15% in its energy consumption for one, recirculate air cools faster and greater the fresh air intake, greater the time taken to cool it, leading to an increase in fares as well.

It may not be possible or wise at this point for India to put curbs on import of critical Chinese consumer goods, at least nonessential goods like toys can be banned to make a beginning. We must also liberalise foreign investment in our economy, especially by western countries as well as Japan, Korea, and others with whom we have friendly relations. We must walk the talk by being less bureaucratic to make ease of doing business with us a reality.

In practice, complete self-reliance is not even a practical objective for any country no country can produce everything it consumes. A better option is to build an efficient, globally competitive economy. Our size will then ensure that we have economic bargaining power. Perhaps we should also develop alternative sources of supply of crucial inputs to insure against any external blackmail.

Taxes and subsidies are methods of income distribution in a welfare state. All taxes and no subsidies are only ideal, not humanitarian. ‘Taxes for revenue’ argument cannot be justified when there is drastic reduction in purchasing power and for the public, no viable affordable products are made available. Better to have tax caps so that disparate distortions can be avoided in the economy.

A Baseline Frame Work for Indian States to Manage the Health Crisis

State Governments in India will need to be specific and innovative in their immediate reactions to health crisis. To effectively curtailing this Pandemic, state governments are advised to work together with other private organizations and other development departments.

- Set up national response centres: Governments, with the aligned participation of the private organizations and other major stakeholders, have created or district response centres under the leadership of the Deputy Commissioners to coordinate and manage their immediate reactions during emergency. These centres are showing the leadership and administrative skills, organizational and managerial strength and digital instruments giving various leaders the best opportunities of getting ahead of events when it arises. However, the contribution of the private sector both in diagnostic laboratories and case management is still wanting as they are demanding fee structure which most Indian population cannot afford ranging from a minimum of Rs 15,0000 to 50,000+ per day. Most of the advisors to the national and State governments are either popular private sector clinicians, the role of public Health professionals is overlooked.

- Earlier recognition and proper management the health crisis: Governments are pursuing holistic and comprehensive approach to manage and reduce the curve of the pandemic intensifying efforts to ensure both physical and social distancing through travel restrictions, curfews and lockdowns as well as larger-scale monitoring to test cases and ensure contact tracing. However, the governments are not yet ready for a potentially upsurge in number of cases, which will require higher numbers of testing facilities, beds in isolation centres, ventilators and other medical tools and supplies, including more healthcare givers.

- Secure food supply and essential services: The state governments are effectively managing food supply chains, especially food products of regular needs and ensure proper regulation and pricing of these food products for accessibility and affordability. Adequate access to essential services such as telecoms, portable water supply scheme, power supply system and other basic utilities are also ensured

- Adequate provision for the most vulnerable populations: This includes taking proper steps to protect workforce and provide essential services for the affected communities, particularly the most vulnerable people in the societies, through social safety and stimulus packages; including provisions of palliatives, house to house cash support and cash transfers are being well managed so far.

- Managing the impact on the economy: Governments are recognizing the likely effect of this pandemic on their economy and businesses through series of analysis and offer both long-term and short-term stimulus palliatives to maintain financial stability and help businesses pull through the crisis especially the Medium and small industries where their products are in high demand. Due to reduction in tax revenue generation, governments are trying to reduce unnecessary spending.

Actions for the Private Sector in India

The primary duty of private-sector organizations is to ensure continuity of services during any crisis. I suggest four strategic dimensions as discussed below:

- Protect workers: Ensures job protection and guarantee continuation of employment in a safe work environment and preserve the employees’ health through health guidelines and safe working healthcare facilities and strict isolation of suspected cases.

- Regularize supply chains: Industries and organizations need to ensure continual conduct of business through transparent supplier engagement, demand assessment, and adjustments of production and operations.

- Engage customers: Companies need to establish crisis communication and identify the necessary changes to key market strategies and policies, ranging from guidelines and policies to sustain social distancing, waivers of cancellation and rebooking fees.

- Stress-test financials: Organizations need to create and evaluate significant impact of the crisis using epidemiological, social, and economic perspectives to address and project working capital requirements. There is need to point out areas for cost reduction and containment of expenditure across the business. Actions for Development Organizations Development partners are supporting Indian government in their battle against Covid- 19, most experts suggest the following actions by them:

- World Health organization in technical support, UNICEF in creating awareness need to work with the Governments both at national and state and district levels to make good decisions in order to provide emergency response during the crisis, meet the needs of the people and ensure sustainability of healthcare and economic systems. They can ensure regular importing of Rapid diagnostic kits for improving COVID 19 lab tests to international level.

- Development organizations like the World Bank, bilateral agencies like BMGF, can support financial partnership.

- Establish new financial mechanisms to support businesses in India through financial bond, insurance, cash support, and more. Designing financial-support models for small and informal businesses is sacrosanct, as well as for households.

- Help States and districts in strengthening healthcare systems for universal health care, as many basic services have been disturbed since March 2020. The biggest challenge to the primary health care system is planning for reviving Health and Welfare Centre to provide comprehensive health care as envisaged in NHP 2017. It may be worth for the development partners to work with the district teams and develop a model comprehensive PHC service plans and support aggressive implementation and monitor the outcomes in at least one district in each state

Conclusion

“While a valuable debate about whether India has the fiscal room to afford a substantial stimulus is taking place, it’s important to note that the size of India’s support program is by far the lowest, as a percentage of GDP, among the top 10 global economies.” If policymakers make it abundantly clear that unconventional policies will be time- and event-specific, and would be unwound once its objectives are achieved, I think financial macro stability will not be affected. On the brighter side, investors could also start focusing on whether economic growth can return in the medium term should a targeted fiscal package be able to contain the immediate downside [1].

Most experts believe that the economic recovery will be gradual because a certain amount of physical distancing will continue over the medium term to avoid another wave of infection. In turn, this will cause an uneven recovery across different sectors. Businesses that depend on the gathering of people, such as retail, hospitality, tourism, cinemas, exhibitions, and construction sites, may see on going restrictions and weaker activity. On the other hand, sectors that cater to social distancing, including personal mobility, packaged foods, telecom, and home improvement, automation, white goods, and consumer electronics, are likely to recover faster.

Government reforms have bolstered the formal sector over the past few years; however, income levels in the informal areas have suffered as a result. Credit growth among nonbanking financial companies has steadily declined due to a freeze in the wholesale money market during most of 2019. This has affected overall credit growth, particularly in the informal sector. Unless the economy is supported by adequate stimulus measures from the government, the sudden stop in economic activity will affect income and savings. The fiscal measures that focus on the long term should include [16].

A. Reduction of corporate tax rates on new investments to incentivize capital formation and attract foreign investment. B. The removal of the dividend distribution tax to encourage private sector investment. C. A simplified personal income regime with reduced rates-a move that is in line with the streamlining of the tax code. D. Expansion of the PM-KISAN scheme, which directly transfers money to farmers in a targeted way. E. Higher spending on long-term initiatives, such as rural roads, irrigation, warehousing, and transportation, to improve the productivity of the economy.

Most economists in India argue that with these fundamental building blocks in place, India has a unique opportunity to revitalize economic growth through Atma Nirbhar Program that should include the “3Rs”: Recycle-Funding government spending needs through the privatization of state-owned enterprise assets. Rebuild- Aggregating savings by providing tax cuts to the private sector and households. Reinvest-Providing incentives for manufacturing firms to reinvest such savings to substitute imports and increase the country’s global market share of exports. Majority believe the 3Rs would help address India’s cyclical growth challenges through higher government spending, increased savings for the private sector and households, and create more job opportunities by encouraging new investment. Some elements like recycling (the privatization of state-owned enterprises) may get delayed. In many industrialist and economist view, policymakers will need to adopt innovative solutions to bridge the gap, they can find through increased government spending and other policy measures. Indian policymakers are in a relatively good position to accomplish this due to the country’s ample foreign exchange reserves and the low level of short-term foreign debt, which lends to a robust capital account. In addition, the country’s inflation outlook remains benign. The sharp correction in crude oil prices should remain a key positive catalyst for markets, as India is a large importer of crude oil. India will benefit from a lower import bill and improved current account balance. This translates into higher domestic savings and provides room for the RBI to remain accommodative, as a US$40 fall in oil prices could result in approximately US$50 billion of total savings. Overall, the COVID-19 pandemic will accelerate the formalization-led growth story that underpins our long- term bullishness on Indian equities. The listed market, which is represented by the organized sector, should emerge more robustly and gain market share. In the current environment, most economist believe the following type of companies and sectors are likely to succeed:

A. Sectors include personal mobility plays (two-wheelers), home automation and improvement plays (consumer electronics, white goods, decorative paints), personal hygiene products, packaged foods, and telecom. B. Import substitution plays benefiting from government policy of encouraging domestic manufacturing (electronics manufacturing services companies), as well as a diversification of production away from China due to the trade war. It is also expected that select information technology service and exports will benefit as they are enabling remote working across the globe. C. Some experts believe that companies like leisure and travel, hospitality, and commercial real estate are less likely to succeed. Companies with high fixed costs and debt on their balance sheet should face a disproportionate downgrade risk and threat of closure.

Most experts believe that India remains a growth story that is local, defensive, and its exports have a good opportunity to gain global market share.

References

-

Ministry of Health & family Welfare, GOI, Covid data Updates-NHM, MOH &FW New Delhi.

-

(2020) WHO Coronavirus Disease (COVID-19).

-

(2020) COVID-19 pandemic in India.

-

(2020) Times of india Bengaluru, Delhi.

-

CDC adds three new symptoms to the COVID list.

-

(2020) GVA impact from COVID-19 across India.

-

Consumer Price Index (2020) Ministry of statistics and programme implementation, government of India, National statistical office.

-

David R Curry (2020) Center for Vaccine Ethics and Policy, Vaccines and Global Health.

-

(2020) Impact of Covid-19 Pandemic on Labour Supply and Gross Value Added in India’ Indira Gandhi Institute of Development Research (IGIDR), India.

-

(2020) India’s unemployment rate, the Centre for Monitoring Indian Economy (CMIE) on 1 July 2020, GOI.

-

(2020) Covid-19: Are India, others testing enough to get a true measure of spread? Business World.

-

(2020) World Health Organization. Coronavirus disease (COVID-19) Technical Guidance: Infection Prevention and Control.

-

David E, Mead O (2020) The Economic Impact of COVID-19 in Low- and Middle-Income Countries Analysis. Centre for Global Development.

-

McKinsey and Company (2020) COVID-19: Implications for business.

-

(2020) GST Collections for June 2020 Lower Than That in Last Year.

-

(2020) India: The long-term outlook remains compelling, despite notable short-term challenges, Rana Gupta, Manulife investment management.

-

(2020) COVID-19 response for Pharma companies- Respond. Recover. Thrive.

- Capacity Constraints in Pediatric Inpatient Psychiatric Care: A Cross-Sectional Analysis of Bed Availability and Geographic Access in North Carolina

- Why Healthcare Analytics Still Optimizes the Wrong Things

- Coding, Coverage, and Care: The Infrastructure of Transgender Health Inequities

- The Effect of Classroom Attendance on Academic Achievement of Management and Leadership Discipline of Nursing Students at Instituto Superior Cristal and Universidade de Dili, Timor-Leste, 2024: A Case Study

- The Role of Social Bonds in Facilitating Shared Investments and Resource Allocation: Addressing the “Wrong Pocket Problem” in Public Health and Healthcare

- Social-Cultural Factors Contributing to Antimicrobial Resistance in Livestock Farmers and Community Households in Kayonza District, Rwanda