The Paradox of the Dark Side of Leadership Creativity: Analyzing Creative Pursuits, Ethical Decision-Making, and Organizational Downfalls through the Cases of Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers

This journal focuses on the leadership behaviors, creative strategies, and unethical decisions of individuals such as Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers. The study aims to understand how leadership creativity can be misused or unethically applied and its implications for organizations. The research design involves a secondary data desk review, analyzing case studies of these individuals to identify patterns and examine the misuse of creativity and subsequent ethical breaches. By exploring the transformation of initially ingenious ideas into detrimental outcomes, the study sheds light on the concept of the “dark side of creativity” and discovers patterns in leadership decisionmaking and characteristics that contributed to the downfall of the leaders and the organization. The research concludes that ethical decision-making is essential to harnessing the positive potential of creativity. It underscores the importance of ethical leadership, transparency, and stakeholder trust for long-term organizational sustainability. By prioritizing ethics and balancing creative pursuits with ethical considerations, leaders can enhance their effectiveness and promote organizational success. This study contributes to our understanding of the relationship between creativity, ethics, and leadership effectiveness. It emphasizes the significance of responsible decision-making and ethical behavior in utilizing creativity for positive organizational outcomes. The findings have implications for organizational practices, highlighting the importance of ethical leadership, transparent governance, and responsible decision-making processes in fostering long-term success and maintaining stakeholder trust.

Introduction

Today, the first thing that springs to mind when hearing the names Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers is fraud and financial crises, but this was not always the case. These individuals were once considered successful CEOs who were praised for their perceived business acumen and had significant influence over investors, employees, and even national economies. However, their actions ultimately led to severe negative consequences for many people and prompted significant legal and regulatory reforms globally. The actions of these individuals not only caused significant financial losses for investors but also had far-reaching impacts on economies, employees, and public trust in the financial system. As a result, laws and regulations were implemented globally to prevent and detect fraudulent activities, strengthen corporate governance, and protect investors. These scandals serve as reminders of the importance of transparency, ethical behavior, and effective oversight in the business world.

But then one wonders whether the ingenuity introduced by these leaders, which was once lauded, can now be classified as dark creativity, as is often done by some people in the corporate world lately. Furthermore, how do the creative pursuits and ethical decision-making processes of leaders, exemplified by the cases of Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers, explain the paradoxical nature of leadership creativity, and what implications does this have for organizational outcomes?

Significance of the Research

The significance of this research lies in its examination of leadership creativity applied unethically and its impact on organizations. By analyzing the cases of Ponzi, Andersen, Madoff, and Ebbers, the research seeks to highlight the potential consequences when creativity is misused or lacks ethical constraints. The findings are expected to reveal patterns of how creativity was misused in the cases of Ponzi, Andersen, Madoff, and Ebbers, shedding light on the factors that facilitated their unethical actions. The outcomes of this research will have implications for organizational practices, emphasizing the importance of ethical leadership, transparent governance, and responsible decision-making processes.

Literature Review

This literature review aims to explore and examine the inherent paradoxes in leadership creativity, providing insights for leaders to understand the risks and opportunities associated with creative pursuits. By analyzing prominent cases involving Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers, this review initiates discussions on the paradoxes of creativity and sheds light on their implications. The review is divided into two main sections: the analysis of these notable cases and the examination of the darker aspects of creativity, emphasizing the crucial role of leaders in ensuring accountability for organizational sustainability. It highlights the significance of ethical decision-making, stakeholder well-being, and comprehensive due diligence in creative strategies to prevent profound consequences. Furthermore, this review challenges the notion that ethics is solely a personal matter, emphasizing the intrinsic relationship between ethics and effective management, thereby promoting a comprehensive perspective on ethics and its impact on organizational success and stakeholder well-being.

Charles Ponzi Creative Pursuits, Ethical Decision- Making, and Downfall of Securities Exchange Company as Narrated by Probasco, (2022) Charles Ponzi, born in Lugo, Italy, in 1882, embarked on a journey to the United States at the age of 21, seeking a better life. After working various jobs, including as a postal worker, Ponzi arrived in Boston in November 1903. He claimed in his autobiography, “The Rise of Mr. Ponzi,” that he left Italy with $200 but arrived in America with only $2.50. He moved to different cities, such as Pittsburgh, New York, New Haven, and Providence, before settling in Montreal, Canada, where he worked as a bank teller [1]. While working at the bank, Ponzi witnessed a scheme that would later be known as the Ponzi scheme. The bank faced financial difficulties due to failed real estate loans. The bank’s founder, Luigi “Louis” Zarossi, attempted to sustain it by using customer deposits from newly opened accounts to cover interest payments. However, the bank ultimately failed, and Zarossi fled to Mexico with a significant portion of the bank’s funds. Ponzi experienced hardship following the bank’s collapse and was subsequently caught and imprisoned in Canada for attempting to forge a check made payable to himself.

Upon his release in 1911, Ponzi returned to the United States. By 1919, he was residing in Boston and had begun developing various schemes to make money. It was during this time that he discovered the International Reply to Coupon (IRC), created by the United States Postal Service (USPS). The IRC allowed senders to pre-purchase postage and include it in their letters, which recipients in other countries could exchange for airmail postage stamps to send their replies. Ponzi encountered the IRC when he received a letter from a Spanish business correspondent who had purchased the coupon for 30 centavos. In the US, the same IRC could be exchanged for five cents, making it more valuable due to the weakening Spanish peseta against the dollar. In 1920, Ponzi established Securities Exchange Co., through which he bought large quantities of IRCs from struggling European economies and sold them at higher prices in the US, resulting in substantial profits. However, Ponzi deviated from the legal operation of arbitrage and turned his business into a scam. He persuaded people to invest in his company with promises of additional 50 percent interest within 90 days, which enticed many investors. Ponzi deceived them by claiming to have an extensive network of agents in Europe who could purchase IRCs in bulk and generate profits in the U.S. Instead of using new investor funds to purchase more IRCs, Ponzi kept a portion for himself and paid the rest to earlier investors. This process, known as “robbing Peter to pay Paul,” sustained the scheme as reinvestments from satisfied investors kept it going.

When the Boston Post published a feature on Ponzi’s wealth, the US Post Office Department adjusted the conversion rates for IRCs, disrupting Ponzi’s business model. To maintain the scheme, Ponzi resorted to his “Rob Peter to pay Paul” approach. However, suspicions arose, and investigations were initiated. The Boston Post’s investigation generated negative publicity, causing Ponzi to decline new investments, and triggering a run by investors. Eventually, Ponzi’s office was raided, and he was convicted on federal charges of mail fraud, serving 3½ years in prison. After his parole, he faced state charges, fled on bail, was apprehended, and returned to prison until 1934 [1]. Collectively, Ponzi’s investors lost an estimated $20 million, which totals roughly $280 million in today’s money [2].

Kenneth Lay (CEO later becoming Chairman of Enron), Jeffrey Skilling (CEO of Enron after Kenneth Lay became Chairman), Andrew Fastow (CFO of Enron), and Arthur Andersen’s (Auditors for Enron) Creative Pursuits, Ethical Decision-Making, and Downfall of Enron Corp as narrated by Segal, (2016) Kenneth Lay, Jeffrey Skilling, and Arthur Andersen implemented specific strategies and practices at Enron that created the perception of a highly successful company before the Enron scandal. Enron Corp.’s tale portrays a company that achieved remarkable success only to experience a rapid and catastrophic collapse. The downfall had far- reaching consequences, affecting numerous employees and significantly impacting Wall Street. At the pinnacle of Enron’s success, its shares were valued at $90.75. However, just before declaring bankruptcy on December 2, 2001, they had plummeted to a mere $0.26. Even today, many marvel at how such a formidable business, once among the largest in the United States, disintegrated almost instantaneously.

Enron was established in 1985 through the merger of Houston Natural Gas Co. and Inter North Inc., a company based in Omaha, Nebraska. Following the merger, Kenneth Lay, who had previously served as the chief executive officer (CEO) of Houston Natural Gas, assumed the roles of CEO and chairman at Enron. Lay swiftly transformed Enron into an energy trading and supply company. With the deregulation of energy markets allowing companies to speculate on future prices, Enron positioned itself to seize the opportunity. In 1990, Lay founded Enron Finance Corp. and handpicked Jeffrey Skilling, an impressive consultant from McKinsey & Co., to lead the newly formed corporation. Skilling’s early contribution was transitioning Enron’s accounting approach from the traditional historical cost method to the mark-to- market (MTM) accounting method, which received official approval from the U.S. Securities and Exchange Commission (SEC) in 1992. MTM is a means of evaluating the fair value of accounts, such as assets and liabilities, that can fluctuate over time. It aims to provide an accurate assessment of an institution’s or company’s current financial position and is widely accepted as a legitimate practice. However, in certain instances, the method can be manipulated since it relies on “fair value” rather than “actual” cost, which is more challenging to ascertain. Some believe that MTM marked the beginning of the end for Enron, as it allowed the organization to record estimated profits as actual profits.

In October 1999, Enron established EnronOnline (EOL), an electronic trading platform dedicated to commodities. Enron served as the counterparty in every transaction on EOL, acting either as the buyer or the seller. Enron leveraged its reputation, credit, and expertise in the energy sector to attract participants and trading partners. The company received acclaim for its expansions and ambitious projects, earning the title of “America’s Most Innovative Company” by Fortune for six consecutive years from 1996 to 2001. Another significant player in the Enron scandal, alongside Fastow, was Arthur Andersen LLP, the accounting firm responsible for Enron’s financial records. Partner David B. Duncan oversaw Enron’s accounts. Andersen, one of the five largest accounting firms in the United States at the time, had a reputation for upholding high standards and practicing quality risk management. However, despite Enron’s questionable accounting practices, Arthur Andersen provided its seal of approval by endorsing the corporate reports for years. Here are some key elements of their creative contributions:

Aggressive Financial Engineering: Jeffrey Skilling and other executives built a complicated financial engineering system. This required the deployment of novel financial tools, including special purpose entities (SPEs) and off- balance-sheet transactions. Enron was able to conceal debt and artificially inflate earnings because of these innovative arrangements. Enron presented a more attractive financial image to investors and stakeholders by removing debt and financial commitments from the company’s balance sheet.

Mark-to-Market Accounting: Skilling also used mark-to- market accounting, which enabled Enron to rapidly record projected future profits from long-term contracts. This accounting practice allowed Enron to record significant profitability on its financial accounts, despite the fact that the gains were frequently based on estimates rather than realized revenue. Mark-to-market accounting was crucial in boosting Enron’s reported earnings and providing the impression of a thriving corporation.

Illusion of Diversification: Enron presented itself as a diverse energy corporation active in a variety of industries, including trading, transmission, and power generation. Skilling highlighted the company’s creative and cutting-edge business strategy, which was mainly based on trading energy commodities. Enron positioned itself as a technology-driven corporation that could profit from energy market instability.

This depiction of variety and technological skill contributed to the impression of a thriving and forward-thinking corporation.

Questionable Partnerships: Enron formed alliances with other companies, including the formation of off-balance- sheet SPEs like the notorious Chewco and Raptors. These joint ventures were used to falsify financial accounts, conceal debt, and exaggerate earnings. These partnerships’ intricate structures and transactions were meant to provide the illusion of financial success and expansion.

By the autumn of 2000, Enron had begun to crumble under its own weight. Skilling concealed the financial losses of the trading business and other company operations using mark-to-market (MTM) accounting. This accounting method allowed Enron to write off unprofitable activities without negatively impacting its financial standing. The adoption of MTM accounting led to deceptive schemes aimed at hiding losses and presenting a more profitable image of the company. To tackle the growing liabilities, Andrew Fastow, a rising star promoted to chief financial officer (CFO) in 1998, devised a deliberate plan to portray the company as financially sound despite the losses incurred by its subsidiaries. Fastow, along with others at Enron, orchestrated a scheme that involved using off-balance-sheet special purpose vehicles (SPVs) or special purpose entities (SPEs) to conceal Enron’s significant debt and toxic assets from investors and creditors. The primary objective of these SPVs was to obscure accounting realities rather than actual operational performance. Over time, Enron’s stock value declined, and the values of the SPVs plummeted, triggering Enron’s guarantees. By the summer of 2001, Enron was in a downward spiral. Lay, who had retired in February, handed over the CEO position to Skilling. In August 2001, Skilling resigned as CEO, citing personal reasons. Around the same time, analysts downgraded their ratings for Enron’s stock, causing it to reach a 52-week low of $39.95. On October 16, the company reported its first quarterly loss and closed its Raptor I SPV, which drew attention from the U.S. Securities and Exchange Commission (SEC). Shortly after, Enron changed pension plan administrators, effectively preventing employees from selling their shares for at least 30 days. Following these events, the SEC announced an investigation into Enron and the SPVs created by Fastow, leading to Fastow’s immediate termination. Additionally, the company restated its earnings dating back to 1997, revealing losses of $591 million and $690 million in debt by the end of 2000. The final blow came when Dynegy, a company that had previously announced a merger with Enron, backed out of the deal on November 28. On December 2, 2001, Enron filed for bankruptcy.

Arthur Andersen, Enron’s accounting firm, was among the first casualties of the scandal. In June 2002, the firm was found guilty of obstructing justice by destroying Enron’s financial documents to conceal them from the SEC. Although the conviction was later overturned on appeal, the scandal deeply tarnished the firm’s reputation, leading it to dwindle into a holding company. Several Enron executives faced charges of conspiracy, insider trading, and securities fraud. Lay, the founder and former CEO, was convicted on six counts of fraud and conspiracy, as well as four counts of bank fraud. Prior to his sentencing, Lay passed away from a heart attack in Colorado. Fastow, Enron’s former CFO, pleaded guilty to two counts of wire fraud and securities fraud for his involvement in facilitating corrupt business practices at Enron. He cooperated with federal authorities and served more than five years in prison before being released in 2011. Skilling, Enron’s former CEO, received the most severe sentence among all those implicated in the scandal. In 2006, Skilling was convicted of conspiracy, fraud, and insider trading. Initially sentenced to 17½ years, his term was later reduced by 14 years in 2013 [3]. As part of the revised agreement, Skilling was required to contribute $42 million to the victims of the Enron fraud. From 2004 to 2011, the company paid its creditors over $21.7 billion, with the final payout occurring in May 2011.

Bernie Madoff’s Creative Pursuits, Ethical Decision- Making, and Downfall of Bernard L Madoff Investment Securities LLC as narrated by Morris, (2023) Bernie Madoff, a financier, confessed to orchestrating the largest Ponzi scheme in history, defrauding numerous investors, including celebrities like John Malkovich and Kevin Bacon, out of billions of dollars. He transformed his wealth management business, Bernard L. Madoff Investment Securities LLC, into a fraudulent scheme that used money from new investors to pay off earlier investors, disguising it as legitimate profits from a genuine business. Madoff established his penny stock brokerage in 1960, which grew to become one of the largest market makers and operated as a third-market trading business. He subsequently became the chairman of the National Association of Securities Dealers Automated Quotations (NASDAQ) Stock Market. Additionally, Madoff was an active political donor, contributing almost $240,000 to federal candidates, parties, and committees, with a majority going to the Democratic Party. Within his business, Madoff involved family members, with his brother Peter Madoff serving as the senior managing director and chief compliance officer, his niece Shana Madoff as the rules and compliance officer, and his sons Mark Madoff and Andrew Madoff holding positions in the company. As the global financial crisis hit in December 2008, Madoff’s fraudulent operations started to falter as investors sought to withdraw their funds. At that point, he confessed to his sons that the entire enterprise was built on deception and essentially operated as a massive Ponzi scheme.

His sons promptly reported the situation to the FBI, leading to an investigation. Madoff admitted that there was no innocent explanation, acknowledging that he had used incoming investors’ funds to pay off existing ones, resulting in a business that had been insolvent for years. He had lost over $50 billion and had not invested the funds as promised. On December 11, 2008, Madoff was arrested and charged with multiple federal felonies, including securities fraud, wire fraud, money laundering, and perjury. In his guilty plea, he confessed that the fraudulent activities had been ongoing since the early 1990s and that the money received from clients had not been invested as claimed but rather deposited into a bank account. In June 2009, Madoff received the maximum sentence of 150 years in federal prison. During the sentencing, Judge Denny Chin characterized the fraud as extraordinarily evil, unprecedented, and staggering. Madoff expressed remorse, acknowledging the pain and suffering he had caused and leaving a legacy of shame for his family and grandchildren.

Bernard J. Ebbers’s Creative Pursuits, Ethical Decision- Making, and Downfall of WorldCom, Inc. as narrated in the court documents (United States District Court for the Southern District of New York v. Bernard J. Ebbers, 2005) WorldCom, Inc., once a major telecommunications company, filed for bankruptcy in 2002 despite having reached a peak market capitalization of over $180 billion in the summer of 1999. However, from at least September 2000 to June 2002, Bernard J. Ebbers, the CEO of WorldCom, along with CFO Scott D. Sullivan and other top executives, engaged in a fraudulent scheme to hide the company’s deteriorating financial performance. Ebbers actively participated in the scheme by making numerous false adjustments and entries in WorldCom’s financial records, often amounting to hundreds of millions of dollars. These manipulations were done to create the illusion that the company’s quarterly and annual financial results met the expectations of Wall Street. In some cases, these expectations were based on financial targets set by Ebbers himself, knowing that they couldn’t be achieved through legitimate means. Additionally, Ebbers made false and misleading public statements about WorldCom’s financial condition and performance.

As a result of the undisclosed and improper adjustments made by Ebbers and others, WorldCom significantly overstated its reported income by at least $9 billion during the period of the fraud. When the fraudulent scheme was revealed in late June 2002, the price of WorldCom’s stock plummeted further, causing additional losses for shareholders. Ebbers’ actions violated various provisions of the federal securities laws, including antifraud, books and records, and internal control provisions. Furthermore, he aided and abetted WorldCom’s violations of reporting, books and records, and internal control provisions under the federal securities laws.

Creative Strategy: Hailed Until Something Goes Wrong

Creative strategies have long been celebrated as innovative approaches that drive success and growth in various domains, from business to finance and beyond [4]. These strategies are often praised for their ability to disrupt traditional practices and unlock new possibilities. Creswell, et al. [5] assert that, although hardly a household name, the creative strategies of Bernie Madoff for instance “secured a longstanding role as an elder statesman on Wall Street, allowing him to land on important boards and commissions where his opinions helped shape securities regulations. Along the way, he snared a coveted spot as the chairman of a major stock exchange, Nasdaq”. The stories of individuals like Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers serve as cautionary tales of creative strategies that were initially hailed but eventually led to catastrophic consequences. These individuals implemented innovative and seemingly successful approaches, garnering admiration, and accolades for their achievements [5]. However, their creative strategies eventually led to negative outcomes, revealing the unethical and fraudulent practices behind their apparent success. The reasons these individuals, like many others in organizations today, are compelled to sidestep ethical principles in pursuit of creative strategy for money or fame are echoed by Marc Barry, an expert in competitive intelligence, who remarked that, “As a CEO, do you honestly believe your shareholders are concerned about whether you’re Billy Buttercup or not? (...) I highly doubt it. People want money, plain and simple. That’s what matters in the end” [6, 7]. The prevailing corporate culture, tainted by greed and moral apathy, has created an environment where leaders face escalating pressure to relentlessly drive shareholder value, irrespective of the consequences [7]. In this fiercely competitive landscape, leaders are compelled to explore creative tactics to impress shareholders and board members, safeguarding their positions to consolidate power and perpetuating the illusion of their esteemed status [7].

Understanding the Paradoxes of Creativity

To succeed in today’s highly competitive business landscape, organizations must proactively foster a culture of creativity and innovation. A key catalyst for innovation lies in the presence of creative and innovative individuals within the workforce. However, realizing the full potential of these creative minds necessitates a paradigm shift in leadership and organizational management [8]. The concept of the “Creativity Paradox” sheds light on the complex interplay between creativity and societal regulations [8]. While creativity is generally viewed as advantageous, it carries a paradoxical nature. Eric Bonetto, the lead author of the scientific paper titled “The Creativity Paradox” in the journal New Ideas in Psychology, underscores the challenges associated with being creative, particularly in social contexts governed by established norms, rules, and culture [8]. In certain environments, novel and innovative ideas may face resistance or even sanctions due to their deviation from the status quo. Embracing creativity demands not only recognizing its potential but also cultivating a supportive and open-minded atmosphere, such as by providing some level of autonomy that embraces unconventional ideas, even if they challenge prevailing conventions [8].

While autonomy is crucial for empowerment and encouraging creativity in organizations, it must be accompanied by an appropriate level of control. Empowerment does not imply a complete absence of structure or accountability. Rather, it involves striking a delicate balance [8]. By establishing clear objectives, boundaries, and guidelines, organizations enable creative individuals to channel their energy effectively without veering too far from the organization’s overarching vision [8]. This controlled autonomy provides a framework within which they can freely express their creativity while working collaboratively towards shared goals [8].

Factors Contributing to Unethical Choices

It is natural to wonder why leaders like Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers didn’t focus on using their creative strategies to ethically grow their businesses. It is both perplexing and unfortunately common to witness the misapplication of good creative strategies in pursuit of unethical gains when a straightforward and ethical approach could have been chosen. Unethical behaviors such as stealing, deception, cheating, fraud, and aggression can stem from individual, issue-specific, and environmental factors [9]. Researchers Jennifer Kish-Gephart, David Harrison, and Linda Treviño conducted an analysis of 136 academic studies on ethical and unethical choices, identifying three main reasons for unethical behaviors in organizations, which they referred to as “bad apples” (individual reasons), “bad cases” (issue-specific reasons), and “bad barrels” (environmental reasons) [9]. The “bad apples,” or individual reasons for unethical choices, involve individuals who prioritize self- interest and engage in manipulative behaviors for personal gain. They often fail to comprehend the consequences of their actions and believe that ethical choices are dependent on circumstances [9]. Furthermore, such individuals, prior to assuming leadership positions, may comply with unethical instructions from authority figures and act solely to avoid punishment [9].

The “bad cases,” or issue-specific reasons for unethical decisions, arise when certain issues are more likely to result in unethical choices. Leaders are inclined to act unethically when they fail to perceive the immediate harm caused by their actions, such as when the victim is distant or the damage is delayed [9]. Unethical judgments also occur when leaders lack accountability or when there is a lack of checks and balances to detect and condemn misconduct or unethical decisions [9]. The “bad barrels,” or environmental reasons for unethical behavior, occur when a company prioritizes individualistic behavior over the well-being of employees, customers, and the community. Unethical decisions are more likely in such an environment. For instance, a performance management system that solely focuses on individual bottom- line achievements, regardless of how they are attained, can contribute to unethical behavior [9].

Although most leaders profess a desire to uphold the highest ethical standards in their organizations, they may be unaware that their own leadership choices can inadvertently foster unethical decisions [10]. Carucci [10] explains four ways in which leadership choices can encourage unethical behavior:

- Creating a psychologically unsafe environment where people are afraid to speak up, leading to misconduct or collusion to act unethically.

- Applying excessive pressure to achieve unrealistic performance targets.

- Failing to make ethical behavior and integrity a routine part of conversations and activities Leaders should integrate ethics into everyday operations and establish policies and norms that prioritize ethical considerations.

- Acting beyond reproach. Leaders must not only establish standards and policies to prevent unethical behavior but also demonstrate compliance with them. By understanding the underlying reasons for unethical behavior and the influence of leadership choices, leaders can strive to create a culture that fosters ethical decision- making and integrity throughout their organizations.

The Role of Leadership and Accountability

The increasing emphasis on ethics in business and management has prompted scholars to concentrate on ethical leadership behavior [11]. This focus has provided researchers with opportunities to explore methods that enhance knowledge of ethical behavior in organizations, facilitating the development and sustainability of ethical leadership behavior. The volatile nature of today’s global economy presents organizational leaders with complex ethical dilemmas, underscoring the importance of ethical decision-making as a key aspect of leadership behavior. To foster ethical leadership behavior, organizations must reduce the likelihood of leaders engaging in inappropriate conduct [11] by adopting mechanisms that promote ethical leadership behavior. One such mechanism discussed in literature is accountability [11]

Accountability involves assessing the beliefs, feelings, performance, and behavior of both oneself and others [11]. It is a crucial construct for supporting ethical leadership behavior in today’s global economy and is considered central to promoting business ethics [11]. Within organizations, accountability encompasses both self-accountabilities, where leaders hold themselves accountable and develop self- awareness, and other accountability, where leaders perceive others evaluating their behavior [11]. Overall, accountability involves assessing individual beliefs and feelings and evaluating the behavior of oneself and others. It also entails monitoring and evaluating one’s own performance and behavior to mitigate the risk of leaders making unethical decisions that impact employees and shareholders.

Safeguarding Organizational Sustainability

Although the growth or performance of organizations in today’s world requires creativity, the sustainability of an organization cannot be guaranteed without enforcing ethical standards [11]. In the late 1990s, the United States put forward the concept of VUCA (volatility, uncertainty, complexity, and ambiguity) in military management, indicating that the world is facing a paradigm shift in the information age [12]. With the development of the times, leaders in organizations need to develop creative strategies for action in the face of many uncertainties [12]. Implementation of these strategies without ensuring the application of ethics in decision- making or the implementation of ideas will lead to some of the challenges faced by institutions like Enron Corp., Bernard L. Madoff Investment Securities LLC, and WorldCom [11].

Organizational sustainability requires business ethics because organizations are not only important in themselves but also contribute to the growth of the economic system and provide benefits for consumers. Business is often at the core of economic decisions and functional management for progress. Different functional institutions, including businesses, are responsible for producing goods and services and helping to protect and conserve ethics [13]. Businesses require the enforcement of ethics to ensure success and sustainability. Ethics are principles that define what is good and right or bad and wrong and provide a code of behavior for practical definitions [13]. Business ethics provide standards and guidelines for management and stakeholder decision- making. In the absence of such codes, there is often a lack of consensus on appropriate ethical principles. Laws and ethics are related, but ethics enable ethical decision-making. A code of ethics is present in over 90% of sustainable global organizations. Organizational sustainability requires shared values and investments in the future, including building people and society [13]. Business ethics are foundational to organizational sustainability based on economic, environmental, and social conditions in the communities where they operate [13].

Methodology

The purpose of this research design is to conduct a secondary data desk review focused on analyzing case studies [14] of Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers to understand how leadership creativity can be misused or unethically applied and its implications for the organization. The objective is to identify patterns and examine how the creativity of the leaders’ understudy was applied unethically, leading to the respective financial scandals associated with each Leader. The research aims to enhance our understanding [15] of how unethical behaviors or decisions by leaders can transform initially ingenious ideas, intended for organizational growth or sustainability, into detrimental outcomes, which led to the categorization of the once-hailed creative ideas as dark creativity, prompting nations to enact laws prohibiting such practices.

Research Questions

a) How did Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers utilize their creative pursuits unethically? b) What were the common patterns or factors that facilitated the misuse of creativity and the subsequent ethical breaches in their respective cases? c) What were the specific implications of their unethical actions on organizational outcomes and stakeholders?

Data Collection

The research will primarily rely on secondary data sources, particularly case studies, investigative reports, scholarly articles, news articles, and legal documents [14]. These sources will provide in-depth information on the scandals associated with each individual, their creative approaches, and the ethical issues involved.

Data Analysis

The data analysis will involve a systematic review and analysis of the collected secondary data with the aid of Chat AI. The following steps will be followed: a) Thoroughly read and review each case study and relevant sources to understand the details of the scandals, the individuals involved, and their creative pursuits. b) Identify commonalities and patterns across the cases, such as deceptive practices, fraudulent schemes, or unethical decision-making processes. c) Analyze the specific creative strategies employed by each individual and how they were misused for personal gain or to deceive stakeholders. d) Examine the ethical breaches and the consequences they had on organizational outcomes, including financial losses, reputational damage, and regulatory changes. e) Identify key themes, insights, and implications emerging from the analysis.

Ethical Considerations

Given that this research involves the analysis of sensitive and potentially controversial cases, ethical considerations must be addressed. The researcher will adhere to the principles of academic integrity and ensure the proper citation of sources. Additionally, care will be taken to present the findings objectively and avoid personal biases or judgments.

Limitations

The research design acknowledges certain limitations: a) The reliance on secondary data sources may limit the availability and depth of information. b) The analysis may be constrained by the perspectives presented in the selected case studies and sources. c) The research design does not include primary data collection methods, such as interviews or surveys, which may provide additional insights.

Results and Analysis

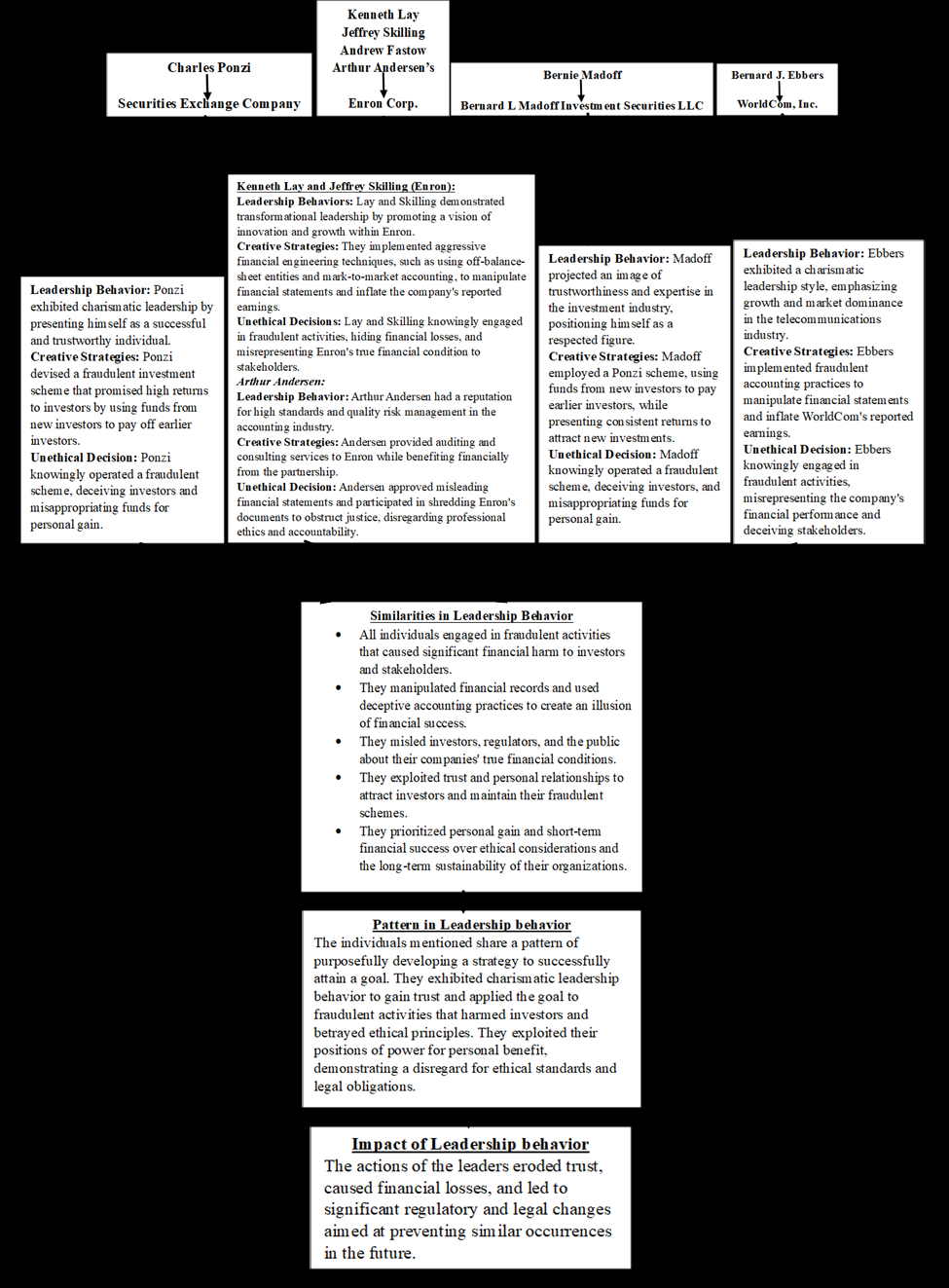

To identify the leadership behavior, unethical decisions, and similarities in the behaviors of Charles Ponzi, Kenneth Lay and Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers, the process and procedure below was followed.

- Researched and Gathered Information: Thorough research was conducted on the Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers, including their backgrounds, roles, and the events surrounding their unethical actions. Information was collected from reliable sources such as court documents, and reputable publications.

- Analyzed Leadership Behavior: The leadership behavior exhibited by each individual was examined. Traits, characteristics, and actions that highlighted their leadership styles, approaches, and influences over others were considered. Aspects such as charisma, persuasion, decision-making, and influence on their organizations were analyzed using the aid of chat AI with leading questions such as “identify leadership behaviour, in Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers behaviour in managing their respective organisations.”

- Identified Unethical Decisions: Specific unethical decisions made by each individual were identified. Focus was placed on actions that violated laws, ethical principles, professional standards, or caused harm to stakeholders. Evidence of fraud, deception, manipulation, or breach of trust was considered using the aid of chat AI with leading questions such as “identify unethical decisions, in Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers behaviors while managing their respective organisations.”

- Compared and Contrasted Behaviors: The leadership behaviors and unethical decisions of Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers were compared. Similarities or patterns that emerged were examined. Common themes, strategies, or methods used to deceive others, manipulate financial information, or gain personal benefits were identified using the aid of chat AI with leading questions such as “identify similarities or similar patterns in their behaviours of Charles Ponzi, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers”.

- Considered the Impact: The impact of their behaviors on stakeholders, including investors, employees, and the public, was evaluated. The extent of financial losses, reputational damage, legal consequences, and the overall fallout resulting from their actions was assessed.

- Drew Conclusions: Based on the analysis, conclusions were drawn about the leadership behavior and unethical decisions of each individual. Shared patterns or similarities in their approaches to deception, fraud, or unethical practices were identified. This included the use of charm, manipulation of financial records, exploitation of trust, or prioritizing personal gain over ethical considerations.

Results

Results of analysis of leadership behavior, unethical decisions, pattern, similarities, and Impact from secondary data collected on the cases of Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers are shown in figure 2.

Analysis

The analysis of the paradox of the dark side of leadership creativity pursuits and ethical judgments of the stated leaders, including Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers, reveals various commonalities and trends in their conduct. These individuals all engaged in fraudulent activities that resulted in significant financial harm to investors and stakeholders. They manipulated financial records and employed deceptive accounting practices to create a false impression of financial success. Moreover, they deceived investors, regulators, and the public about the true financial conditions of their organizations. A key similarity among these individuals is their ability to project charismatic leadership behavior. They presented themselves as trustworthy and successful figures, exploiting trust and personal relationships to attract investors and maintain their fraudulent schemes. By leveraging their charismatic qualities, they gained the confidence and support of investors who believed in their promises of high returns and financial success.

Furthermore, these individuals were motivated by personal financial interests, which led them to prioritize individual advantages and short-term financial success over ethical concerns and the long-term sustainability of their businesses. As a result, they willingly engaged in fraudulent actions, demonstrating contempt for ethical norms and legal responsibilities. The presence of creative strategies in their fraudulent activities is another shared pattern. They implemented various deceptive techniques, such as Ponzi schemes, off-balance-sheet entities, mark-to-market accounting, and fraudulent accounting practices. These strategies allowed them to manipulate financial statements, inflate reported earnings, and create a façade of financial prosperity.

Overall, the research indicates that these individuals exhibited a consistent pattern of charismatic leadership behavior, fraudulent activities, and misapplied creative strategies while disregarding ethical principles in pursuit of wealth and fame or maintaining a false status in society. They exploited their positions of power and trust to deceive investors and stakeholders, ultimately causing substantial financial harm.

Discussion

The discussion highlights the leadership behaviors, creative strategies, and unethical decisions of five individuals: Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers. The cases provide important insights into the consequences of disregarding ethical considerations in the pursuit of creativity and organizational success. While these individuals demonstrated creative strategies to enhance organizational performance, their unethical decisions had severe repercussions. These individuals were involved in fraudulent activities that caused significant financial harm to investors and stakeholders [1]. They employed deceptive practices, manipulated financial records, and misrepresented their companies’ true financial conditions to create an illusion of success [1]. By exploiting trust and personal relationships, they attracted investors and perpetuated their fraudulent schemes.

One common pattern among these individuals is the use of charismatic leadership behavior to gain trust and credibility. According to Creswell, et al. [5], the Bernie Madoff story offered a remarkable understanding of the mindset of a charismatic leader who cunningly used his talents to victimize his investors by almost $50 billion. It shows how such leaders can easily draw in many successful individuals to their fraudulent scheme. They project an image of success, expertise, and trustworthiness, which allows them to deceive investors and stakeholders effectively. This charismatic leadership style played a crucial role in Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers attracting new investors, keeping regulators out of their business, and maintaining their fraudulent activities for a long time. Creswell, et al. [5] stated that Bernie Madoff, for instance, was “smart in understanding very early on that the more involved you were with regulators, the more successful you are in shaping regulation.” An investigator in Bernie’s case opined that Bernie was very creative in his modus operandi because, despite the fact that he ran a Ponzi scheme and Charles Ponzi had made regulators aware of such schemes, regulators could still not detect his fraudulent acts. He was cited in Creswell, et al. [5] as having stated that, if you’re very close with regulators, they’re not going to be looking over your shoulders that much. Very smart.” Which shows how he ran a similar strategy to Charles Ponzi, yet regulators could not detect the illegality or fraudulent scheme he was running.

Another common pattern identified was the implementation of creative strategies aimed at making people believe in their expertise and trust them. This pattern is described by Creswell, et al. [5] in the article titled “The Talented Mr. Madoff” as impression management. They assert that people like Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, and Bernhard Ebbers “know what people want, and they give it to them” to create a good and trusting image of themselves in the minds of their stakeholders, including regulators [5]. They employed various techniques, such as fraudulent accounting practices, Ponzi schemes, aggressive financial engineering, and misleading financial statements [5]. These strategies allowed them to manipulate financial records, inflate reported earnings, and attract new investments [9]. However, these creative strategies were ultimately unethical and served the individuals’ personal gain rather than the long-term sustainability of their organizations. They exploited their positions of power, deceived investors, and betrayed ethical principles. In each case, leaders played a pivotal role in promoting and implementing unethical strategies [9]. They either actively participated in or turned a blind eye to fraudulent activities, prioritizing personal gain over ethical decision-making. This highlights the need for leaders to be ethically responsible, act as role models, and promote a culture of integrity and ethical behavior throughout the organization [11]. Leaders must balance the pursuit of creativity and innovation with a strong commitment to ethical values [11].

Implications of the Research

The implications of these cases for organizational outcomes are twofold. First, they highlight the importance of integrating ethics and morality into leadership practices [11]. Leaders must not only be creative and innovative but also act ethically and responsibly [11]. Organizations need to foster a culture that values and rewards ethical behavior and holds leaders accountable for their actions [11]. Second, these cases emphasize the need for effective oversight and governance mechanisms within organizations [8]. Strong internal controls, independent audits, and regulatory frameworks are essential to detecting and preventing fraudulent activities. Organizations should establish mechanisms to promote transparency, accountability, and ethical decision-making at all levels Fola. By recognizing the dark side of leadership creativity and its potential consequences, organizations can take proactive measures to mitigate risks and promote responsible leadership. This includes fostering a culture of ethics, implementing robust governance structures, and prioritizing transparency and accountability [8]. Such measures can help prevent future instances of unethical behavior and safeguard organizational outcomes and stakeholders’ trust.

Recommendations for future studies

Future research in this area could focus on preventative measures such as enhancing corporate governance, improving regulatory frameworks, and promoting ethical leadership practices to mitigate the risks associated with such fraudulent activities. Other specific recommendations for research are as follows:

- Comparative analysis: Conducting a comparative analysis of additional case studies involving individuals or organizations that demonstrate a balance between creativity and ethical considerations. This would provide a broader understanding of how ethical leadership practices can contribute to long-term organizational sustainability while promoting creativity.

- Ethical frameworks and guidelines: Developing and exploring specific ethical frameworks and guidelines tailored to creative industries or organizations that heavily rely on innovation This research could focus on identifying best practices for integrating ethical considerations into creative decision-making processes and establishing accountability mechanisms.

- Organizational culture and ethics: Investigating the impact of organizational culture on ethical decision- making and the effective integration of creativity and ethics This research could explore how fostering a culture that values ethical behavior and promotes open dialogue can positively influence creative processes and outcomes.

- Stakeholder perception and trust: Examining the role of stakeholder perception and trust in the context of creativity and ethics This research could delve into the factors that influence stakeholders’ perceptions of ethical leadership and how it impacts their trust in organizations, as well as the potential long-term consequences for organizations that prioritize creativity over ethical considerations.

- Long-term effects of ethical leadership: Conducting longitudinal studies to analyze the long-term effects of ethical leadership on organizational sustainability, employee engagement, stakeholder trust, and financial performance. This research could provide insights into the lasting benefits of ethical decision-making and its impact on various aspects of organizational success.

- Education and training: Investigating the role of education and training in fostering ethical leadership skills among creative professionals This research could explore the effectiveness of integrating ethics education into creative curricula or providing specialized training programs to promote responsible and ethical creative practices.

- Cross-cultural analysis: Conducting cross-cultural studies to explore how cultural factors influence the balance between creativity and ethical considerations in different regions or countries. This research could highlight cultural nuances and provide insights into developing culturally sensitive approaches to ethical leadership in the creative industries.

- Industry-wide initiatives: Examining industry-wide initiatives and collaborative efforts to promote ethical behavior and responsible creativity This research could explore the effectiveness of self-regulation, industry standards, and certifications in promoting ethical practices and shaping a culture of responsibility within the creative industries.

By pursuing these avenues of research, a deeper understanding of the complex relationship between creativity, ethical leadership, and long-term organizational sustainability can be achieved. This knowledge can inform the development of practical strategies and interventions to foster responsible and ethically driven creativity in various organizational contexts.

Conclusion

The case study of leaders such as Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers provided valuable insights into the relationship between creativity, leadership behaviors, unethical decision-making and long-term organizational sustainability. These individuals exhibited leadership behaviors that often-projected charisma, innovation, and a focus on growth. However, their creative strategies were aimed at sustaining the illusion of success or attracting new investments, ultimately leading to unethical decisions and behaviors. This study emphasizes the significance of the consequences that arise when ethical considerations are disregarded in the pursuit of creativity. Some specific conclusions reached through the examination of the leadership practices of Charles Ponzi, Kenneth Lay, Jeffrey Skilling, Arthur Andersen, Bernie Madoff, and Bernhard Ebbers are:

- The Dark Side of Creativity: The case study revealed the dark side of creativity, where leaders utilized their creative ideas and strategies in unethical or harmful ways. The individuals in question employed their creative talents to manipulate stakeholders, engage in fraudulent activities, and misappropriate funds for personal gain. This highlights the potential negative consequences that can arise when creativity is unchecked.

- The Paradox of Creativity: The paradox of creativity arose when the leaders utilized their creative talents to drive organizational growth and success, but their unethical decisions undermined the very foundation of sustainable and effective leadership. In this case study, the individuals’ unethical behaviors contradicted their creative and growth-oriented strategies, leading to a paradox where their creativity did not contribute to long-term organizational sustainability.

- Long-Term Organizational Sustainability: The case study emphasized that sustainable organizational success is closely tied to ethical leadership. Leaders who prioritize ethical considerations, transparency, and stakeholder trust are more likely to achieve long-term organizational sustainability. The individuals’ disregard for ethical considerations in pursuit of personal or organizational benefits ultimately undermined the long- term sustainability of their organizations.

- Leadership Effectiveness: Effective leadership entails more than just charisma and creativity. It requires leaders to make ethical decisions, exhibit integrity, and balance creativity with ethical considerations. The case study demonstrated that the individuals’ manipulation, deceit, and disregard for ethics hindered their effectiveness as leaders, leading to the downfall of their organizations and loss of stakeholder trust [16, 17, 18, 19, 20].

This research emphasizes the neutrality of creativity itself, as its ethical considerations determine its outcomes. While some have labeled negative outcomes of creative pursuits as “dark creativity,” this study asserts that creativity, in its essence, is neutral and characterized by originality and ingenuity, devoid of inherent evil. It is the unethical application of creativity that leads to negative outcomes. Describing the negative aspect as the “dark side of creativity” better acknowledges its nature.

References

-

Probasco J (2022) Who was Charles Ponzi? What did he create? Investopedia.

-

Cohler A (2017) The Evolution and Impacts of the Ponzi Scheme and Governmental Oversight. Ramapo College Honor’s Symposium: pp: 1-25.

-

Segal T (2016) Enron scandal: The fall of a Wall Street darling. Investopedia.

-

Cvetanovski B, Jojart O, Gregg B, Hazan E, Perrey J (2021) The growth triple play: Creativity, analytics, and purpose. McKinsey & Company.

-

Creswell J, Thomas L (2009) The talented Mr. Madoff. The New York Times.

-

Kuhn A (2020) Corporate Psychopaths and their effect on leadership and corporate culture. University of Graz pp: 1-132.

-

Bakan J (2005) The Corporation: The pathological pursuit of profit and power. Simon & Schuster.

-

Fola V (2023) The creative paradox: Effective leadership in a creative environment. LinkedIn.

-

Tobah B, Fischhoff M (2022) 3 reasons employees act unethically. Network for Business Sustainability (NBS).

-

Carucci R (2016) Leadership Strategy: Four Ways Your Leadership May Be Encouraging Unethical Behavior. Forbes.

-

Ghanem K, Castelli P (2019) Accountability and Moral Competence Promote Ethical Leadership. Journal of Values-Based Leadership 12(1).

-

He S, Yun X (2022) Research on the influencing mechanism of paradoxical leadership on unethical pro- supervisor behavior. Behavioral Sciences 12(7): 231.

-

Ugoani JN (2019) Business ethics and its effect on organizational sustainability. Global Journal of Social Sciences Studies 5(2): 119-131.

-

Reddy KS, Agrawal R (2012) Designing case studies from secondary sources – A conceptual framework. SSRN Electronic Journal.

-

Wickham AOCN R (2019) Secondary analysis research. J Adv Pract Oncol 10(4): 395-400.

-

Balasubramanian N (2011) Corporate governance - By Robert A. G. Monks and Nell Minow. Corporate Governance: An International Review 20(1): 119-120.

-

International banker (2021) Charles Ponzi (1920) International Banker.

-

Morris L (2023) What did Bernie Madoff do? True story of Netflix’s monster of Wall Street. Radio Times | TV, film and entertainment news - Radio Times.

-

Small J (2023) Who was Charles Ponzi? The shocking story behind the scheme. Entrepreneur.

-

Bernard V, Ebbers J (2005) United States District Court for the Southern District of New York. Securities and Exchange Commission pp: 1-16.

- Occupational Stress and Mental Health Outcomes Among Police Officers: A Mini Review

- The Experience of Counterproductive Leadership on Mental Health and Impact on Retention in U.S. Marines: A Phenomenological Study

- Nomophobia in the Digital Age: A Study on College and University Students

- Emotional Regulation in Children with Autism and Learning Disabilities

- Antisemitism on American College Campuses and Its Impact on Jewish Students

- Exploring the Role of Empathy in the Associations of Family Functioning and Purpose in Life with Attitude towards Abortion among Undergraduates: A Moderation Analysis