Transition Risks in a Small Open Economy: An EDSGE Model with Blue Firms, Financial Frictions and Macroprudential Policy

While mitigation and adaptation measures are effective in fighting climate change, there are transition risks linked to these efforts that can impact output. However, the right mix of policies can help to alleviate transition risks, thereby mitigating the associated economic impact. This study explores the economic effects of a carbon tax in an economy featuring “blue firms” that capture carbon. Extending Carattini, et al. we develop a dynamic stochastic general equilibrium (DSGE) model with financial frictions and macroprudential policy, integrating blue firms with brown (polluting) and green firms. The results show that macroprudential policy mitigates transition risks, and blue firms enable a smoother economic shift under a carbon tax, enhancing welfare by up to 5.34% in the combined model. To note, the findings also reveal that while macroprudential policies can dampen credit cycles and reduce volatility, they do not substitute for environmental regulation.

Abbrevations

DSGE: Dynamic Stochastic General Equilibrium; E-DSGE: Environmental Dynamic Stochastic General Equilibrium; DICE: Dynamic Integrated Model of Climate and the Economy; Bernanke, BGG: Gertler and Gilchfist; SIDs: Small Island Developing States; RBC: Real Business Cycle; ESG: Social and Governance; CSA: Climate Scenario Analysis; TNC: The Nature Conservancy.

Introduction

As the threat of climate change intensifies [1, 2], policymakers as well as governments around the world are turning to carbon taxation as a market-based instrument to reduce greenhouse gas emissions. While ambitious climate policies, such as carbon taxes and emissions regulations, are vital to mitigating global warming, their implementation often entails significant economic adjustments known as transition risks. These risks refer to the potential for abrupt changes in asset values, investment patterns and overall macroeconomic stability, as economies shift away from carbon intensive activities. As economies move toward more sustainable practices, the economic effects of such policies have become important, particularly within the context of their associated impact in small open economies.

Equally, countries have placed considerable emphasis on how transition risks can be mitigated. This can be achieved either through the use of counterbalancing fiscal and monetary policies, or through the presence of new or existing activity that assists with carbon neutrality. In particular, “blue firms”, which are companies that specialize in capturing and storing carbon, have gained traction in recent times, and are considered to have a positive effect on climate fighting initiatives through their ability to reduce emissions, revitalize the economy, and improve livelihoods and jobs [3].

There is a growing body of literature that explores climate change, climate policy and the impact of climatic events on the macroeconomic landscape. While the physical effects of climate change are relatively easy to measure, transitional risks are often less visible and therefore more difficult to assess. Transitional risks also tend to lag, as policies take time to come into effect, while physical impacts occur in real time and have lasting effects on output [4]. Recent studies examine the role of green and blue firms in shaping transition risks associated with climate change, offering insights into how these risks can be estimated. This research draws on several scholarly studies that explore the economic effects of a carbon tax in an economy including “blue firms”.

Carattini, et al. [2] develop a dynamic stochastic general equilibrium (DSGE) model that incorporates environmental externalities and financial frictions to analyze the macroeconomic implications of climate policy. The model is calibrated using parameters that mirror the US economy, and the simulations consider economies both with and without financial frictions to assess the role of financial stability. The authors conduct two sets of simulations: first, they examine the short-run response of the economy to the introduction of a carbon tax, alongside the role of macroprudential policies to mitigate adverse effects. Second, the authors solve for the efficient policy response to a carbon tax in both the steady state (long-run) and in response to business cycles driven by exogenous productivity shocks.

The findings suggest that ambitious climate policy can in fact trigger financial instability; however, the implementation of macroprudential policies can help to offset the impact of the policy. In particular, the implementation of a carbon tax in an economy with financial frictions can cause a reduction in investment in both green and brown firms, as the tax lowers the market value of carbon-intensive assets, and this forces banks to have to cut lending to all firms, due to their exposure to these assets. However, the imposition of macroprudential policies that shift banks’ portfolios away from brown firms and into green firms can help to offset this risk. If banks are less exposed to brown assets, the imposition of a carbon tax will not impact the asset value of their portfolio as much, and they therefore will not have to cut or suspend their net lending. Further, the authors found that the first- best outcome for the steady state is the implementation of macroprudential policy, which alleviates the transition risk associated with a carbon tax.

Building on the framework developed by Carattini, et al. [2], Ding, et al. [5] analyze how non-homothetic energy consumption preferences interact with carbon markets to effect carbon emissions and macroeconomic outcomes. The study addresses whether macroeconomic policy tools interact meaningfully with carbon markets. To this end, the authors develop an environmental dynamic stochastic general equilibrium (E-DSGE) model, which encompasses six sectors: households; intermediate product producers; and final product producers; carbon market; central bank with non-homothetic consumption preference; and government with non-homothetic consumption preference.

The findings reveal that carbon pricing behavior driven by the carbon market will impact the implementation effect of policy mixes and changes in household welfare, and this impact will vary based on non-homothetic preferences. In particular, the authors found that a positive shock to carbon prices can reduce emissions. Furthermore, when monetary policy includes carbon reduction objectives, it can reinforce the decline in emissions through the interest rate channel, as tighter monetary conditions suppress aggregate demand and output. Finally, the degree of non-homothetic preferences will determine how much it accelerates the transmission path of policies, as well as the relative size of welfare effects in the short and long-term.

Moreover, despite Ding, et al. [5] contributions, the study is constrained by several limitations. Most notably, its heavy reliance on U.S. specific data reduces the model’s applicability to developing economies, where energy consumption patterns and institutional contexts differ. Additionally, the model is theory-based, and lacks empirical validation, since it was not tested against observed emission reductions from real-world policy contributions.

In another strand of related literature, authors look at the effect of carbon sink trading in achieving economic and environmental benefits. Carbon sinks help to absorb carbon dioxide from the atmosphere, and as such, they help to reduce the overall level of greenhouse gas from the air. The impact of carbon sink trading on the macroeconomic landscape, based on impulse responses is explored by Xu, et al. [6] who also examine the influencing factors by way of a sensitivity analysis. The authors also use welfare analysis to assess the impact on financial market performance. To make their estimates, Xu, et al. [6] construct an ‘economic- financial-environmental’ framework through a DSGE model, combined with a dynamic integrated model of climate and the economy (DICE), to account for the carbon cycle mechanism. The authors introduce financial accelerators by using the Bernanke, Gertler and Gilchfist (BGG) model, which include capital producers, entrepreneurs, financial intermediaries and other departments.

In their findings, they show that ocean carbon sink trading can improve climate outcomes and social welfare under efficient carbon sinks. Further, they find that the efficiency of carbon sinks has a significant impact on environmental benefits, while carbon sink prices are seen to have a less significant impact. As for the financial accelerator effect, the findings reveal that the loss of social welfare is compounded by a decrease in output, driven by an exogenous shock in the financial market. Similar to Ding, et al. [5] the study is constrained by limited data, since empirical calibration is based on national data from China, which cannot be applicable from a global perspective.

Though relevant, these studies are subject to limitations deriving from their simplified representation of the financial system and transition risk. While financial frictions are modelled through a banking sector exposed to carbon- intensive assets, real-world financial systems involve a broader range of institutions-such as insurance companies and credit unions—and a more complex set of financial instruments. Further, representing transition risk solely through carbon taxation overlooks the politically constrained nature of policy transitions. Henceforth, future studies would benefit from more analyses on blue activity, as the authors only consider brown firms.

This paper contributes to the existing body of literature by applying a dynamic stochastic general equilibrium model (DSGE), following Carratini [2] to the Bahamian context—one of the countries that is most vulnerable to climate change. It represents the first study of its kind conducted for The Bahamas, thereby expanding a limited body of literature on transition risks in small island developing states (SIDs).

Specifically, this study aims to examine the transition risk of climate policy, and determine how this risk can be mitigated through the use of other policy measures. A DSGE model that integrates both environmental externalities and financial frictions and assess how these frictions affect the optimal nature of transition risk was developed. The study shows that financial frictions significantly alter the transition dynamics following the introduction of a carbon tax. In particular, constrained firms reduce investments more sharply, leading to amplified output losses and a slower reallocation of capital across sectors. These effects raise concerns about the short-run macroeconomic costs of climate action in financially fragile environments. Second, the role of macroprudential policy, which is modeled as a tax on bank assets, in stabilizing these dynamics was assessed. While such tools can dampen credit cycles and reduce volatility, they do not substitute for environmental regulation. Lastly, the impact of blue firm activity, which offsets the impact of climate change by reducing emissions was examined. Blue firms are seen to have a positive impact on output, and alleviate transition risks by enabling a smoother transition following a carbon tax, and enhancing overall welfare. The results underscore a need for coordinated policy design that jointly addresses climate externalities and financial distortions, particularly during the transition to a low-carbon economy.

The remainder of this paper is organized as follows: section II presents an overview of stylized facts to give context to the key themes in the model, while section III details the methodology for how the DSGE model was calibrated. Section IV presents a thorough discussion of the results and section V proposes a set of policy recommendations, before concluding in section VI.

Stylized Facts

Blue, green, and brown firms represent distinct approaches to business operations with different levels of environmental impact, sustainability, and resource utilization. Blue economies, like The Bahamas, are centered around industries that make sustainable use of oceanic resources, seas, and coastal areas for economic growth, improved welfare, and generate employment. Given its geographical location and heavy reliance on coastal sectors, The Bahamas is among the most climate-vulnerable ocean-based economies, facing significant risks from hurricanes, biodiversity loss, and rising sea levels [7]. These firms encompass industries such as renewable energy, fisheries, tourism, and maritime transportation which are essential in addressing challenges of climate change and biodiversity loss [8]. Similarly, green firms adopt principles of environmental sustainability in their operations, strive to use renewable resources, and attempt to minimize the negative environmental impacts of their activities [9]. In contrast, brown firms pertain to industries driven by economic growth and dependent on environmentally destructive activities, such as oil extraction, heavy metal processing, coal mining, and burning of fossil fuels [10]. These firms harm biodiversity and lead to environmental sustainability challenges. This section explores key stylized facts regarding these firms’ trends, their challenges, and their roles in fostering a sustainable future.

Blue Firms

The blue economy is a rapidly growing sector with opportunities for economic, environmental, and social growth. This section highlights key stylized facts about blue firms, focusing on regional vulnerabilities, global significance, and emerging opportunities, with particular attention to The Bahamas and the Caribbean:

- Global Growth and Economic Impact. The blue sector is valued at approximately USD 24 trillion and is projected to grow at a faster rate than the global economy between 2010 and 2030 [3]. Blue firms have made substantial contributions to global food security, human welfare, and economic development. Ocean economies have also absorbed 25% of extra C02 in the atmosphere to mitigate climate change [11].

- Sectoral Significance: Fisheries and Trade. The fisheries industry alone supports the livelihoods of an estimated 660-820 million people worldwide. Seafood has become one of the highest-valued trade commodities, accounting for USD 139 billion in 2013 [11]. However, poor fisheries management is a persistent global issue that results in revenue losses of up to USD 80 billion annually [8].

- There are policy gaps in blue economy legislation. Of the 54 commonwealth nations, only Mozambique, The Bahamas, and Belize have introduced legislation specifically focused on blue economy sectors. Mozambique enacted a comprehensive Sea Law, while The Bahamas and Belize are in the process of developing similar legal frameworks [12].

- Vulnerabilities within the Caribbean. Blue economy sectors have contributed up to 18% of total GDP in the Caribbean region [11]. However, the development of blue firms has been significantly impacted by global recessions triggered by the COVID-19 pandemic and exposure to natural disasters. Due to their small size and geographical location, Caribbean countries are considered among the most at-risk globally in terms of blue economy resilience [13]. The pandemic particularly affected the tourism sector, with tourist arrivals to The Bahamas falling by 70% in March 2020, compared to March 2019 [13].

- Underdeveloped Renewable energy. Ocean renewable energy is a critical pillar of sustainable blue economies but remains limited in The Bahamas. Renewable energy sources account for less than 0.1% of the country’s total electricity generation [3]. The only documented renewable installation is a photovoltaic microgrid with a capacity of 402kW, located on Ragged Island.

- Emerging Opportunities in Aquaculture. Despite being underdeveloped, aquaculture and marine biotechnology in The Bahamas represent high-valued opportunities within the blue economy. While aquaculture remains constrained by limited production scale, the harvesting of Bahamian soft coral has successfully generated an estimated USD 3-4 million annually for cosmetic lines that use it in their bio-products [13].

Green Firms

The stylized facts synthesize recent empirical trends and forecasts related to the green economy, sectoral transformation, and labour markets. Collectively, they highlight the growing importance of green firms in the global and regional economic landscape:

- Energy production, transportation, and finance sectors are focal sectors in the green economy.

- Energy and transport are the first and second largest carbon emitters globally, while the finance sector is being reformed to enable the green transition. Demand for green skills in these sectors grew by 15.2% between February 2022 and 2023 [14].

- Green skills are growing fastest in carbon-intensive industries. Between 2016 and 2023, green skill concentration in the oil and gas sector rose by 21%, while EV-related skills among auto workers grew by a median 61% [14].

- SIDS are experiencing green transitions, particularly in transport. For example, in The Bahamas, EV sales surged by 133% between 2020 and 2021, reflecting early momentum toward transport decarbonization [15].

- Green jobs are among the most in-demand roles in major economies. Europe anticipates 4 million new jobs in the solar energy sector by 2050, driven by its clean energy transition [16].

- Global green job growth is accelerating. The International Labour Organization estimates 24 million green jobs will exist globally by 2030, representing 14% of total U.S. jobs. In the first quarter of 2024 alone, the U.S. green economy recorded 43,841 jobs across nearly 10,000 employers [17, 18].

- Heat stress is an emerging threat to productivity and employment in the green economy. Rising global heat stress may reduce total working hours by 2.2% and cut global GDP by USD 2.4 trillion in 2030, equivalent to 80 million full-time jobs lost. This is consistent with USD 280 billion in losses recorded in 1995 [19].

Brown Firms

While brown firms have historically driven economic growth, they pose more challenges to the sustainability goals that green firms seek to develop. The stylized facts capture trends in economic growth, employment, and environmental impact:

- Brown firms are a significant source of global energy supply. According to the 2023 Energy Institute report, fossil fuels jobs accounted for 82% of global energy supply [20]. Further, of total energy, oil made up 32%; coal, 26%; natural gas, 23%; hydroelectric, 6%; other renewables, 8%; and nuclear, 4% [21].

- Brown firms receive large global subsidies. In 2022, the fossil fuel industry received one of the highest subsidies at USD 7 trillion due to spikes in energy prices caused by the Russian-Ukraine war. This equates to 7.1% of global GDP. China, the United States, Russia, the European Union, and India are the largest subsidizers for these firms [22].

- Brown firms are labour sparse when compared to green firms. The U.K. Energy Research Centre discovered that renewable energy creates three times as many jobs per million pounds compared to fossil fuels [23]. The job multiplier from renewable-based technologies is the largest compared to coal and natural gas which have the lowest multipliers. Net job gains are observed when countries transition from 2020 to 2040 because of increased solar and wind capacity, gains in energy efficiency, and reduced reliance on fossil fuels [24]. Hence, brown firms have the comparative disadvantage with employment.

- In sum, these patterns suggest that blue, green, and brown firms each present both positive and negative implications for the economy. Blue firms contribute significantly to GDP growth, particularly in SIDS, where they serve as key economic drivers despite geographical vulnerabilities. Green firms, among the fastest-growing sectors globally, aim to enhance environmental sustainability through cleaner operations. In contrast, while brown firms remain essential to the expansion of the global energy supply, they pose substantial threats to environmental sustainability.

Methodology

Model

The DSGE model in this study includes households, the central bank (which is also responsible for macroprudential policy) and three types of firms: brown firms, green firms and blue firms. Similar to the model introduced by Carattini, et al. [2] the stock of pollution and financial frictions are introduced as sources of inefficiency. Households optimise their utility – including consumption, labour supply and pollution. The central bank uses prudential tools such as firms’ cost of borrowing to regulate carbon emissions (i.e., penalizing brown firms for emissions and incentivizing green firms).

For the baseline DSGE, there are two firm types that produce brown and green output, with brown firms involving carbon emissions as a byproduct, while green firms do not. Both types of firms operate with the following Cobb-Douglas production functions:

1 ab ab b b b Y AK L − =

1 g a a a g g a Y AK L − =

where 𝐴 is technology, and 𝑎𝑏, 𝑎𝑔 are capital shares, 𝐾𝑏, 𝐾𝑔 are capital stocks, and 𝐿𝑏, 𝐿𝑔 are labor inputs of brown and green firms, respectively.

Per Carattini, et al. [2] pollution has a negative impact on productivity, and emissions are a byproduct of production in the brown sector. The pollution stock (𝑋𝑡) is ( ) 1 , 1 ..., t x t b b t world X X Y δ φ φ + = − + + + where 𝛿𝑥 is decay rate, 𝜙𝑏 𝑌𝑏,𝑡 is brown emisisons and 𝜙𝑤𝑜𝑟𝑙𝑑 is exogenous.

The household utility maximization problem is ∞

( ) , , , 1 , max t t t t Ct Lt t o Eo U C L X β = − ∑

subject to budget and labour constraints t b g L L L = +

Moreover, pollution negatively affects productivity and reduces output according to

1 1-dX )AK eff ab ab b t b b Y L − =

Blue firms are introduced to the model, represented by the following Cobb-Douglas production function:

1 au au u u u Y AK L − =

where 𝑢 is the blue sector, and subject to the following constraints:

b g u total K K K K + + =

b g u total L L L L + + = As blue firms are carbon-capturing, the stock of pollution is modified according to ( ) 1 , , 1 t x t b b t u t world X X Y Y δ φ ω φ + = − + − + with 𝜔𝑌𝑢,𝑡 as captured carbon (𝜔 is efficiency). With the modified pollution stock, as efficiency increases. Hence, the more efficient that blue firms are in capturing carbon, the more they reduce pollution (𝜔 is also linked to the output of blue firms).

To measure how pollution impacts firms’ access to the financial system and how they react to changes in policy, the following financial friction is introduced to the model: Firms borrow at:

, k i i R R spread = +

( ) i i i spread f lev M = +

where leverage is:

D lev N = , i t i i t ,

Finally, macroprudential tools are also introduced. As monetary policy in The Bahamas is weak, macroprudential policies would be more effective.

Spread rule i i i spread lev M = Γ −

with 𝑀𝑏 > 0 (brown penalty) and 𝑀𝑔 < 0 (green support)

Capital Adequacy

, , 1 i i t i t K N ν + ≤

Under these conditions, brown firms incur a penalty for pollution while green firms are incentivized.

The overall DSGE system integrates households, firms (brown, green, blue), financial frictions, macroprudential tools, and pollution dynamics and is solved in equilibrium.

| Parameter | Value | Meaning |

|---|---|---|

| 𝛽 | 0.9975 | Discount factor |

| 𝜂 | 2 | Risk aversion |

| 𝜉 | 1 | Frisch elasticity of labour |

| 𝜛 | 8.9544 | Labour disutility |

| 𝜌𝐿 | 1 | Intrasectoral CES of labour hours |

| 𝛼𝑏 | 0.35 | Capital share (brown production) |

| 𝛼𝑔 | 0.33 | Capital share (green production) |

| 𝜌𝑌 | 2 | CES between green, blue and brown outputs |

| 𝛼𝑌𝑔 | 0.668 | % share of green output |

| 𝛼𝑌𝑏 | 1 − 𝛼𝑌𝑔 | % share of brown output |

| 𝛿𝑏 | 0.025 | % Capital depreciation rate |

| 𝛿𝑔 | 0.025 | % Capital depreciation rate |

| 𝜙 | 10 | Investment adjustment cost |

| 𝜃1 | 0.0334 | Abatement cost function parameters |

| 𝜃2 | 2.6 | Abatement cost function parameters |

| damage_scale | 0.986 | Environmental damage parameter |

| 𝑑0 | -0.026 | Environmental damage parameter |

| 𝑑1 | 3.61E-05 | Environmental damage parameter |

| 𝑑2 | 1.44E+08 | Environmental damage parameter |

| 𝑑2 | 𝑑2/𝑑𝑎𝑚𝑎𝑔𝑒_𝑠𝑐𝑎𝑙𝑒2 | Environmental damage parameter |

| 𝑑1 | 𝑑1/damage_scale | Environmental damage parameter |

| 𝛿𝑋 | 0.9965 | Pollution decay |

| 𝑒𝑟𝑜𝑤 | 2*3.3705 | Emissions in the ROW |

| 𝐴 | 1 | |

| 𝜌𝐴 | 0.95 | Persistence of aggregate TFP shocks |

| 𝜎𝐴 | 0.007 | Std. dev. of innovations to TFP |

Table 1: ** Parameters and calibration values.

Source: Carratini et al (2023) and authors’ calculations. Table 1: Parameters and calibration values.

Calibration

The parameters for this study are calibrated to be consistent with values found in the literature, while also taking into account features of the Bahamian economy and monetary and financial system. The ones in this study (see Table 1) are mainly consistent with those found by Carattini, et al. [2] which are classified as parameters for the standard real business cycle (RBC), climate externalities, and financial frictions. Consequently, the chosen standard values for the subjective discount factor β is 0.9975 (which represents an annualized risk-free rate of 1% in the steady state), the risk aversion parameter, Frisch elasticity of labour supply, and the capital depreciation rate values are also those found by Carattini, et al. [2]. Further, the capital share output values are calibrated to reflect a more capital-intensive brown sector. The values for inter-sectoral elasticity of substitution between labour hours [25] persistence of TFP shocks, investment adjustment costs and the labour disutility parameters are also ones common in literature related to the RBC [26, 27]. The climate externality parameters (abatement cost functions, environmental damage, pollution decay and emissions in the ROW) are calibrated with the same values as found in the Nordhaus [28] version of the DICE model. The financial frictions and macroprudential components of the model are calibrated to reflect features of the Bahamian economy and financial system.

Discussion

In general, the findings reveal that transition risk associated with the implementation of a carbon tax in an economy with financial frictions has an adverse impact; however, the extent of the fallout can be alleviated with the use of macroprudential policy and the presence of blue firms. We make three main observations from the findings. Firstly, blue firms increase output. As can be seen in Table 2, in an economy with blue firms and without financial frictions or macroprudential policy, output, which is depicted as Y, increases by 36.46% when a carbon tax is implemented. This is intuitive, in that blue firms are not affected by the environmental tax, given that their operations do not contain the use of fossil fuels, or any other activity that will produce greenhouse gases. What is more, the imposition of a carbon tax will cause financial institutions to lower their investment in blue and brown firms, and increase their investment in blue firms, which will therefore support an increase in output. When financial frictions are introduced, the increase in output decreases to 26.09%. However, when macroprudential policies are added, the increase in output strengthens by almost 2 percentage points to 27.99%.

| Variable | Blue | FF | FF+Blue | FF+MP | FF+MP+Blue |

|---|---|---|---|---|---|

| C | 36.44% | 51% | 30.38% | 42% | 31.16% |

| Yb | 17.79% | -7.72% | 8.55% | -14.62% | 0.97% |

| Yg | 8.00% | -7.46% | 0.00% | -2.05% | 6.27% |

| Y | 36.46% | -7.48% | 26.09% | -6.94% | 27.99% |

| Kb | 26.88% | -14.60% | 8.29% | -29.45% | -9.90% |

| Kg | 11.99% | -14.48% | -4.28% | -1.82% | 10.61% |

| emis | 17.62% | -7.90% | 8.58% | -14.64% | 0.90% |

| X | -3.46% | -0.90% | -4.12% | -1.70% | -5.32% |

| W | 3.48% | 0.90% | 4.13% | 1.69% | 5.34% |

Table 2: ** Percentage Deviations from the Baseline.

Source: Based on authors’ calculations. Table 2: Percentage Deviations from the Baseline.

Secondly, we observe that blue firms lower pollution (denoted as X) in all of the simulations, with the reduction highest in an economy with financial frictions, macroprudential policy and blue firms, by some 5.32%. In an economy with financial frictions and macroprudential policy, the reduction in pollution is smaller, at 1.70%, indicating then that macroprudential policies alone are not effective in lowering pollution levels. However, the addition of blue firms helps to correct the environmental externalities that cause pollution by offering products and services that reduce greenhouse gas emissions such as carbon sinks. Hence, in an environment with blue firms alone, pollution reduces by 3.46%.

The third observation is that blue firms offer gains in welfare. In an economy with financial frictions and blue firms, welfare gains (denoted as W) increase by 4.13%, which is higher than the 3.48% increase observed in an economy with blue firms alone. However, without blue firms, macroprudential policies in an economy with financial frictions only produce an increase in welfare gains of 1.69%. Therefore, the presence of blue firms appears to be more effective in delivering welfare gains, in that blue firms reduce the level of pollution, which thereby improves the overall environment and thus, welfare of individuals and households.

Based on these observations, we deduce that the most optimal outcome is achieved when there are financial frictions, macroprudential policy and blue firms. In this environment, output increases by 27.99% from the baseline, pollution decreases by 5.32%, and the welfare gain moves higher by 5.34% when compared to the baseline. When a carbon tax is implemented, banks reduce their lending to blue and brown firms, which ultimately decreases output. However, macroprudential policies that drive a shift in investment from the brown sector to the green sector can help to offset this decrease in output. Further, the addition of blue firms can help to improve the level of pollution by reducing emissions, which not only render improvements in output, but overall welfare. What is interesting is that the deviations in pollution appear to be closely correlated with the movement in welfare gains. When pollution decreases in any of the simulations, the welfare increases by nearly the same magnitude. This insinuates that the two share a negative relationship.

Impulse Responses

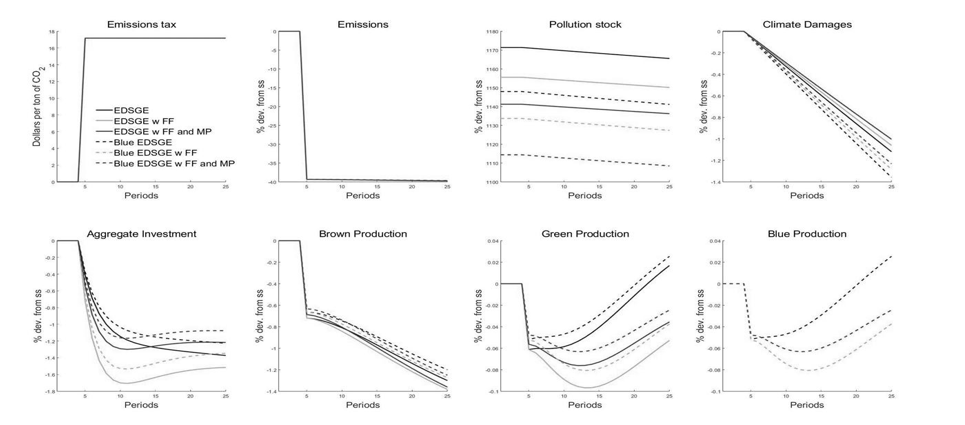

We then examine the dynamic responses of key variables to three policy shocks: a pollution shock, a capital allocation shock and a shock to the pollution stock and climate damages. In the baseline, the impulse response function show that after the imposition of a carbon tax, the level of emissions would remain unchanged in the first 4 periods, and then decline sharply in period 5, and remain low over the long- term (Figure 1). Similarly, climate damages would decline after period 5, with the pollution stock showing a less stark decline over the short- and long-term. Aggregate investment would decline initially, but increase over the long-term, as banks would reduce their lending to brown firms in the short-term, and increase investment in the green and blue sectors over the long-run. This corresponds to the movements registered for brown, green and blue production.

Source: Based on authors’ calculations. Figure 1: Baseline.

We applied a shock to emissions by running the simulations with an increase in the carbon tax from 0.0192 to 0.0288, and a decrease from 0.0192 to 0.0096. When an increase in the carbon tax is applied, the reduction in emissions is most pronounced in the simulation with financial frictions, macroprudential policy and blue firms. The combination of a higher tax, the implementation of macroprudential policies aimed at shifting investment from the brown to the green and blue sectors, and the carbon capture activity of blue firms help to substantiate a sharp and sustained reduction in emissions. Further, the response to a decrease in the carbon tax also features a reduction in emissions, though to a lesser extent when compared to a higher tax, as the production from blue firms help to mitigate the increased emissions associated with the lower tax rate.

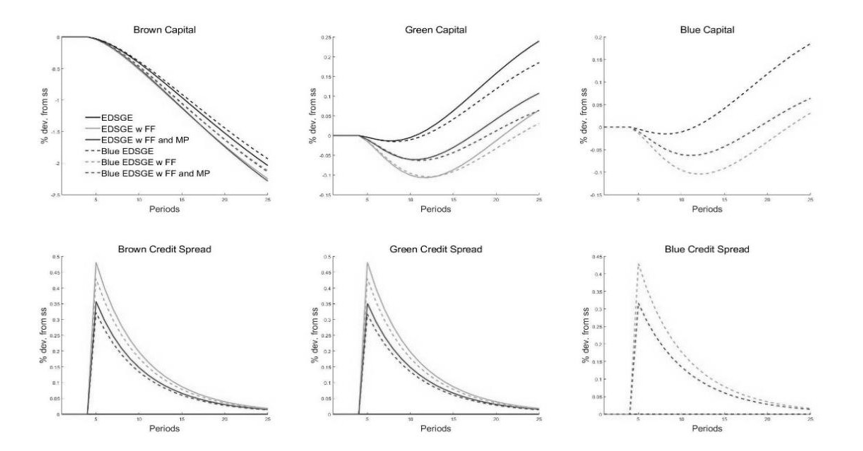

The impulse response from a shock to capital allocation shows what will happen to the stock of capital in brown, green and blue firms in response to a decrease or increase in the carbon tax. Similar to the pollution shock, the responses are most pronounced in the simulation with financial frictions, macroprudential policy and blue firms. An increase in the carbon tax causes banks to redirect investment from brown firms to green and blue firms, which thereby impacts their capital allocations. Therefore, brown capital declines in period 5, and maintains a downward trajectory over the long- term (Figure 2). Simultaneously, the stock of green and blue capital dips initially in periods 5 to 10—reflecting to some extent the impact of the higher tax rate-but increases over the medium to long-term as investment is shifted toward its operations.

Source: Based on authors’ calculations. Figure 2: Capital Allocation Shock.

The third and final shock considers what will happen to the stock of pollution across the different simulations if the pollution decay is adjusted. Increasing the variable for pollution decay raises pollution, thereby amplifying climate damages via the penalty term (1 − 𝑑𝑋𝑡), particularly in the baseline and the model with financial frictions without blue firms. However, a decrease in the variable for pollution decay accelerates decay, and therefore reduces pollution and damages across all variants. This response is most dominant in the simulation with financial frictions, macroprudential policy and blue firms, due to the carbon captured by blue firms. Similarly, raising carbon capture efficiency lowers pollution in blue- inclusive models, with this outcome more marked than in models without blue firms.

In general, the impulse responses underscore the pivotal role of blue firms in mitigating environmental and economic shocks. The model with financial frictions, macroprudential policy and blue firms consistently outperforms the other simulations, balancing emission reductions with capital reallocation and pollution stock control. Macroprudential policy amplifies the carbon tax’s effectiveness by steering resources toward sustainable sectors, while blue firms’ capture efficiency acts as a critical lever for managing pollution. These dynamics suggest that integrating blue firms with policy tools can stabilize the economy during climate policy transitions, a finding robust across tax and parameter shocks.

Welfare Analysis

Welfare is defined as the expected discounted utility of the representative household:

∞ ( ) 0 , , 0 0 1 _t t t t W E U C L X β = = − ∑

where β is the discount factor (0 < β < 1), _Ct_is consumption, _Lt_is labor, and _Xt_is pollution (entering negatively) following the approach outlined by Wei et al. (2023). Welfare gains are computed as:

( ) ( ) variant % 100. / in Welfare Gain W W baseline W baseline = − comparing each variant’s lifetime utility to the baseline EDSGE.

As depicted in Table 3, the welfare gains in a steady state relative to the baseline is minimum when there are only financial frictions, with a gain of only 0.9%. However, when financial frictions are combined with blue firms, which captures the higher carbon, the benefits increased to 4.1%. Further, welfare benefits are at their maximum when combined with financial frictions, monetary policy and blue firms, with a gain of 5.34%. Therefore, the results indicate that the presence of financial frictions, macroprudential policies and efficient carbon tax can contribute to maximum welfare benefits.

The welfare gains reflect the interplay of consumption, leisure, and environmental quality across model variants. In the baseline scenario, the assumption is that there are only brown and green firms, along with a carbon tax, resulting in welfare being constrained by high pollution (X) and limited sectoral flexibility. Therefore, in this scenario, the absence of blue firms, financial frictions (FF) and macroprudential policy (MP), will lead to increased pollution and restraint sectoral activity, thereby impeding welfare.

In the scenario where blue firms are introduced (Blue), welfare is boosted by some 3.5%, underpinned by a 36.4% increase in consumption (C) and 36.5% in output (Y), despite higher emissions of 17.6%. The key driver is the reduction in the pollution stock (X) by 3.5%, through carbon capture, which mitigates climate damages and enhances utility through lower pollution.

What is important to note is that financial frictions (FF) alone yield a modest welfare gain of just 0.9%, with consumption rising sharply by 51.0%, due to altered borrowing dynamics. However, output falls by 7.5%, as credit constraints reduce brown and green production, and pollution reduction is minimal (0.9%), limiting the welfare improvement.

Moreover, combining financial frictions with blue firms (FF+Blue), amplifies welfare beyond including only the blue variant. For instance, consumption grows by approximately 30.4% and output by 26.1%, supported by blue sector activity, while pollution drops further by 4.1%. The synergy of credit constraints and carbon capture enhances environmental quality, outweighing financial frictions output drag.

By incorporating macroprudential policy to financial frictions (MP+FF), it increases welfare by an estimated 1.7%, by redirecting capital away from brown firms toward green and reducing emissions by 14.6%. Consumption also rises by 42.0%, while output declines by 6.9%, owing to a contraction in brown firms, and the reduction inpollution is moderate at 1.7%, without blue firms.

Overall, the full model (FF+MP+Blue) achieves the highest welfare gain of 5.3%, balancing a 31.2% rise in consumption, with a 28.0% growth in output. Brown firms output stabilizes near the baseline at 1.0%, while green firms output grow by 6.3%, and pollution falls by 5.3%, due to blue firms’ capture and macroprudential policy sectoral reallocation. This variant optimizes utility by maximizing consumption and reducing the pollution stock.

Factors Driving Welfare

Examination of the model revealed that welfare improvements stem from three main channels, namely consumption gains, pollution reduction and efficient sectoral allocations. Specifically, for consumption, higher gains in financial frictions (51.0%) and blue firms (36.4%) contributes to an increase economic activity or resource efficiency, directly boosting utility. The second benefit from including financial frictions, macroeconomic policy and blue firms in the framework is the reduction in pollution. Lower pollution reduces climate damages, thereby enhancing output and utility, with blue firms playing a pivotal role. Finally, for the third channel, combining the variants financial frictions and macroprudential policy or financial friction, macroeconomic policy and blue firms will lead to a sectoral reallocation of resources. Specifically, resources will shift to sustainable sectors, mitigating transition costs and supporting long-run welfare. Noteworthy, labor (Lt) adjustments are implicit, but less pronounced, as total labor is constrained, with welfare effects primarily driven by consumption and exports.

Implications

The consolidationoffinancial friction, macroeconomic policy and blue firms(FF+MP+Blue) variants inthe framework result in superior welfare gains, highlighting the value of integrating blue firms with policy tools. Importantly, blue firms alone do not deliver substantial benefits (see Table 3). However, adding financial frictions and macroprudential policy to the mix, leads to maximum environmental and economic outcomes, offering a robust strategy for climate policy transitions. In addition, financial frictions alone, although posting modest gains, without targeted sectoral support, are insufficient to contribute to maximum welfare benefits.

Therefore, from the scenarios presented, the results show that financial friction alone achieves the lowest welfare gain. However, in order to maximize welfare gains, it is necessary to add other variants to the framework (Table 3). In addition, it must be sectoral support-focused, so as to achieve superior welfare advantages. Moreover, combining these variants will translate into a reduction in pollution levels, which will result in further welfare benefits. Overall, the policy mix will convert into positive environmental and economic outcomes, contributing to effective strategy for climate policy transitions.

| Model Variation | Gain vs. Baseline (%) |

|---|---|

| Baseline | 0 |

| Blue | 3.48 |

| FF | 0.9 |

| FF+Blue | 4.12 |

| FF+MP | 1.69 |

| FF+MP+Blue | 5.34 |

Table 3: ** Model Variation.

Source: Based on authors’ calculations. Table 3: Model Variation.

Policy Recommendations

Based on these findings, it is imperative that policies catered toward supporting blue firms are considered at the highest level, and implemented in the short- to medium-term. To this end, we present the following policy recommendations:

Firstly, given that the results confirm that the presence of effective macroprudential policies can help to alleviate the transition risks that follow the implementation of a carbon tax, there is a case to be made for ensuring regulators are approaching their macroprudential policy framework from the right stance. In particular, the more banks are exposed to brown assets, the more adverse the impact of a carbon tax is on their portfolio. However, if regulators employ macroprudential policies such as taxes on firms whose output derive environmental externalities through increased emissions, or subsidies to firms who have environmental, social and governance (ESG) frameworks that actively help to reduce their emissions, this can help to mitigate a deep or prolonged worsening in their asset portfolio in response to climate policy. If banks lend more to firms that are emission reducers, or involved in production that promotes sustainability, their exposure to brown firms will be less, thereby reducing the associated impact of a government tax on brown firms.

Other macroprudential policies that can be considered include implementing loan-to-value ratio caps, and upper limits on the debt service-to-income ratio. As an ex-ante policy, central banks can begin including climate considerations in their macroprudential stress-testing to assess the potential transition and physical risk to the financial system. Examples of this can already be seen in Europe with the Banque de France launching a pilot assessment of banks and insurance companies in 2020, and the Bank of England following in 2021 with an assessment that considered transition and physical risks. In 2023, the United States joined these efforts with the Federal Reserve conducting a pilot climate scenario analysis (CSA) [29] that examined US banks’ ability to measure and manage climate-related financial risks, and have joined other regulators in the jurisdiction to issue guidance on principles for climate-related financial risk management.

To complement this shift in macroprudential policy by regulators, the government can aid in promoting more blue firms over brown firms by unlocking new financing for investment in sustainable activity. Given that the blue economy and firms that specialize in sustainable products or operations are still relatively new, traditional banks have been somewhat conservative in lending to these types of firms. Therefore, to promote more of this activity, the government can partner with multilateral institutions to provide more financing to these firms by either guaranteeing traditional debt issued by commercial banks, or directly providing grants to blue firms. By providing more capital to these firms, they can expand their operations and reduce overall emissions, which can lessen the need for robust climate policy, and that essentially assuages transition risks associated with climate shocks.

Alternatively, the government can also issue blue or green bonds-which have gained prominence in recent years-to raise financing directly for blue activity such as marine conservation, renewable energy, or assisting existing companies in their transition to more sustainable operations. For example, in late 2021, Belize completed a debt conversion of USD 364 million 1 for ocean conversation, making it the world’s single largest debt refinancing for marine conservation to date. In the underlying transactions, the government of Belize repurchased 100% of an existing bond at a 45% discount, and this was financed by The [30] Nature Conservancy (TNC) as a blue loan. The savings from the refinancing is estimated to create approximately USD 180 million in conservation funding over a 20-year period, the proceeds of which will be used to fund conservation efforts, including protecting up to 30% of its ocean resources. As a result of the debt swap, Belize was able to reduce its overall debt level by 12% of GDP. Given that oceans are carbon sinks—which can help to absorb polluting gases from the atmosphere-initiatives like this allow for more investment in activity that will help to reduce emissions, thereby mitigating transition risks [31, 32, 33, 34].

Moreover, for countries like The Bahamas that emit very low levels of greenhouse gases, and house large bodies of water and greenery that act as carbon sinks, the trading of carbon credits can be an efficient and sustainable avenue for raising climate financing. Under the Kyoto Protocol2, all signatory countries are designated emission caps, in line with the overall target of reducing global emissions. However, for countries that produce less emissions than their cap, they are permissible to trade the excess to countries that produce more emissions than their allotment. This then allows the higher emitting countries to maintain their production levels, without driving an overage in the global level of emissions. For countries like The Bahamas, that emits relatively low levels of greenhouse gases, trading carbon credits can be a good source of revenue. In addition, given the mass body of water in the country’s composition, and the land mass of greenery, these carbon sinks can offer

¹ Case Study: Belize Debt Conversion for Marine Conservation - https://www.nature.org/content/dam/tnc/nature/en/documents/TNC- Belize-Debt-Conversion-Case-tudy.pdf ² Kyoto Protocol – An international treaty adopted in 1997 to com- mit industrialized countries to transition to reducing their greenhouse gas emissions inline with agreed targets.

more revenue opportunities, the funds of which can be earmarked to mitigation and adoption efforts that offset the impact of climate shocks.

Furthermore, parallel to supporting blue firms, it is also important to consider policies that will help to drive the transition away from the use of fossil fuels and other activity associated with brown firms, in line with the Paris Agreement3. While financing is paramount to materializing these efforts, there are other policies geared toward mitigation and adaptation that are equally important. In particular, advocating for capacity building through technical assistance from the international community is an essential enabler to achieving climate goals. For example, countries can benefit from knowledge transfers when it comes to developing their energy reform strategies, or drafting legislation for sustainable land use that protects and preserves forests or other carbon sinks. There is also a case to be made for the transfer of technology between countries that promote reduced emissions such as solar power, geothermal energy, and wind mass energy, among others.

Finally, all of these efforts will be mute without international cooperation and collaboration. In this vein, it will be prudent for the government, private sector, multilateral organizations and other international institutions to work cohesively toward the common goal of eradicating the risk of climate change. By mitigating the threat of climate change, the associated transition and physical risk are reduced, thereby limiting the corresponding economic and financial fallout.

Conclusion

This paper explores the complex relationship between climate policy, financial frictions, and transition risk, building on the work of Carattini, et al. [1]. Our analysis, emphasizes that while ambitious climate policies are essential to steer economies toward a sustainable low-carbon outcome, these efforts can produce transition risks, which can have an adverse impact on economic output.

The findings highlight the importance of integrating financial market considerations into climate policy frameworks. Macroprudential policies that reduce informational asymmetries, improve access to green finance, and provide clear, credible signals about the future regulatory environment can help to alleviate financial frictions and mitigate transition risks. Such approaches can facilitate an easier reallocation of capital toward sustainable

³ Paris Agreement – A legally binding international treaty on cli- mate change, championed by the United Nations Framework Convention on Climate Change (UNFCCC).

investments, reducing costs and accelerating the green transition. In addition, the presence of blue firms can help to further mitigate transition risk, but reducing the level of emissions and enhancing overall output, and welfare.

Further, a coordinated effort among policymakers, regulators and financial institutions to develop resilient financial systems that support an efficient transition to lower carbon economy • Acknowledgements: The authors would like to thank Mr. Carlos Madeira, former Visiting Economist at the Bank for International Settlements (BIS) Office of the Americas for his comments on the paper. • Conflict of Interest: The authors declare no conflict of interest. • Disclaimer: The views contained within this paper are the views of the authors and do not reflect the views of the Central Bank of The Bahamas.

References

-

United Nations Climate Change (2025) The Paris Agreement. United Nations Climate Change.

-

Carattini S, Heutel G, Melkadze G (2023) Climate policy, financial frictions and transition risk. Rev Econ Dyn 51: 778-794.

-

Bethel BJ, Buravleva Y, Tang D (2021) Blue economy and blue activities: Opportunities, challenges, and recommendations for The Bahamas. Water 13(10): 1399.

-

Ehlers T, Frost J, Madeira C, Shim I (2025) Macroeconomic impact of extreme weather events (BIS Bulletin No. 98). Bank for International Settlements, Switzerland.

-

Cao J, Ding X, Ma G (2024) The emission-reduction effect of green demand preference in carbon market and macro-environmental policy: A DSGE approach. Sustainability 16(16): 6741.

-

Wei Z, Xu L, Xu Y, Zhou G (2024) Double effect of ocean carbon sink trading and financial support: Analysis based on BGG-DICE-DSGE model. Front Mar Sci 11: 1473828.

-

Aligishiev Z (2025) Assessing climate change risks- Potential output losses and gains from strengthening resilience: The Bahamas (IMF Selected Issues Paper No. SIP/2025/030). International Monetary Fund, USA.

-

World Bank (2017) What is the Blue Economy?. World Bank, USA.

-

Čekanavičius L, Bazytė R, Dičmonaitė A (2014) Green business: Challenges and practices. Ekonomika 93(1): 74-88.

-

Change Oracle (2022) Environmental implications of three types of economies: Brown, blue and green. Change Oracle.

-

World Bank (2016) AMCOECC blue economy development framework: Growing the blue economy to combat poverty and accelerate prosperity. World Bank, USA.

-

Voyer M, Benzaken D, Rambourg C (2022) Institutionalizing the blue economy: An examination of variations and consistencies among Commonwealth countries. Philos Trans R Soc B 377(1854): 20210125.

-

Phang S, March A, Touron-Gardic G, Deane K, Failler P, et al. (2023) A review of the blue economy potential and opportunities in seven Caribbean nations pre-COVID-19. ICES J Mar Sci 80(8): 2233-2245.

-

LinkedIn Economic Graph (2023) Global Green Skills Report 2023. LinkedIn, USA.

-

Hartnell N (2021) Bahamas in world’s eighth largest electric car sale rise. Tribune 242, Bahamas.

-

Timis DA (2023) The future of work in the green economy. World Economic Forum, Switzerland.

-

International Labour Organization (2018) 24 million jobs to open up in the green economy. International Labour Organization, Switzerland.

-

Sederberg R (2024) The green job ecosystem. Lightcast, USA.

-

International Labour Organization (2019) The impact of heat stress on labour productivity and decent work. International Labour Organization, Switzerland.

-

Igini M (2024) Fossil fuel accounted for 82% of global energy mix in 2023 amid record consumption. Earth. Org.

-

Venditti B (2024) Visualizing global energy production in 2023. Visual Capitalist.

-

Black S, Parry I, Vernon-Lin N (2023) Fossil fuel subsidies surged to record $7 trillion. International Monetary Fund, USA.

-

Climate Action (2022) New report finds renewable energy can create three times as many jobs compared to fossil fuels. Climate Action.

-

Kim J, Mohommad A (2022) Jobs impact of green energy (IMF Working Paper No. WP/22/101). International Monetary Fund, USA.

-

Horvath M (2000) Sectoral shocks and aggregate fluctuations. J Monet Econ 45(1): 69-106.

-

Heutel G (2012) How should environmental policy respond to business cycles? Optimal policy under persistent productivity shocks. Rev Econ Dyn 15(2): 244-264.

-

Annicchiarico B, Di Dio F (2015) Environmental policy and macroeconomic dynamics in a new Keynesian model. J Environ Econ Manage 69: 1-21.

-

Nordhaus W (2018) Evolution of modeling of the economics of global warming: Changes in the DICE model, 1992-2017. Clim Change 148(4): 623-640.

-

Board of Governors of the Federal Reserve (2023) Agencies issue principles for climate-related financial risk management for large financial institutions. Federal Reserve, USA.

-

The Nature Conservancy (2022) Case study: Belize debt conversion for marine conservation. The Nature Conservancy, USA.

-

Demekas D, Grippa P (2021) Financial regulation, climate change, and the transition to a low carbon economy: A survey of the issues. International Monetary Fund, USA.

-

Guo L, Jiang X, Wei Z, Xu W, Zhao Z, et al. (2023) Can ocean carbon sink trading achieve economic and environmental benefits? Simulation based on DICE- DSGE model. Environ Sci Pollut Res 30(28): 65393- 65408.

-

Hopper G (2024) The Fed pilot climate scenario analysis exercise: A review. Bank Policy Institute, USA.

-

World Bank (2023) Blue economy development in the Caribbean: A regional policy framework. World Bank, USA.

- Community Forestry Enterprises as a Model for Sustainable Forest Development: The Case Of The "Baja Tarahumara" in Chihuahua, Mexico

- Ecological and Socio-Economic Impacts of Chromolaena odorata and Mesosphaerum suaveolens, Two Invasive Alien Species in Central and Southern Benin, West Africa

- Epigenetic Sustainability: Modeling the Human Factor as a Natural Resource through Science 4.0 and the NR3C1 Biological Pilot

- Growth-at-Risk: A Framework for Assessing Economic Vulnerability

- The Rural Territory as a Socioecological System for the Management of Public Policy for Sustainable Rural Development

- Germination Responses of Araribá (Centrolobium tomentosum - Guillem. ex-Bentham - Fabaceae) when Subjected to Different types of Betterments